Words: 1033 | Estimated Reading Time: 6 minutes | Views: 4583

Apartment prices across the Tokyo metropolitan area have continued to climb, and the traditional site-selection logic that “only locations within the Route 16 loop are safe” is rapidly losing effectiveness. As areas inside the Yamanote Line enter a global-capital pricing band, structurally attractive opportunities increasingly appear “outside the psychological boundary.” Omiya has been reassessed as a core city in this value migration; Urawa provides support as a high-end residential node. Together they form a new asset growth corridor in the northern Tokyo metropolitan area.

From “Tokyo Hinterland” to “Northeast Japan Hub”: The Urban Evolution Logic of Omiya

To understand Omiya’s investment case, we must return to its historical role.

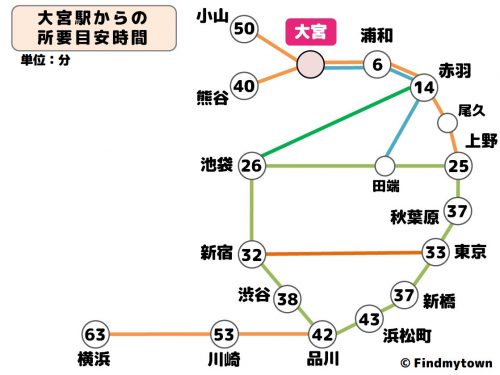

Omiya is not a typical Tokyo bedroom suburb. Since the Meiji-era railway construction, Omiya has functioned as a rail-node city. With the sequential integration of the Tohoku, Joetsu and Hokuriku Shinkansen lines, Omiya became an important transport hub within the JR East network. Today Omiya Station is one of the key nodes of the Shinkansen network in eastern Japan, handling diversion for wide-area commuting and business flows north of Tokyo.

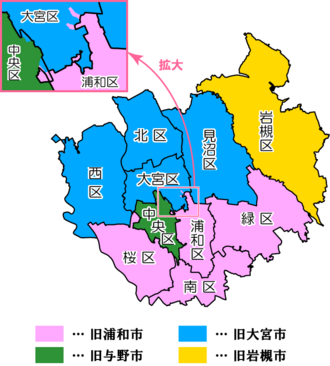

Administratively, Urawa, Omiya and Iwatsuki merged in 2001 to form Saitama City, which was designated a government ordinance-designated city in 2003. This administrative upgrade centralized regional planning and fiscal resources, providing the institutional foundation for subsequent urban redevelopment.

Unlike pure residential sprawl, Omiya’s development path resembles a “sub-center upgrade”:

Strengthening of the rail hub

Concentration of commercial functions

Expansion of office and hotel uses

Ongoing urban renewal

This evolution has gradually shifted Omiya from a “Tokyo commuter station” to a “self-sustaining city.”

Demographics, Prices and Rental Profile: Rebalancing Signals in the Data

Within Urbalytics’ internal monitoring framework, Omiya’s performance does not reflect short-term price volatility but a more structural rebalancing signal. Moving the lens from single transactions to combined indicators—population structure, transaction density and rental absorption capacity—clarifies the logic behind its price appreciation.

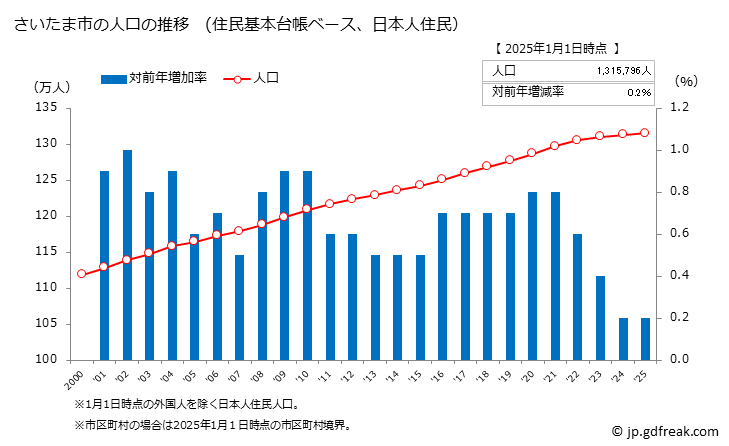

First, population stability and a trend toward younger households. Unlike some peripheral cities experiencing accelerated aging and net outflows, Saitama City’s overall population remains high and continues to show relatively stable net inflows within the Tokyo metro area. At the ward level, Omiya Ward and Chuo Ward have a significantly higher share of family households than surrounding prefectural averages (specific figures forthcoming). This family inflow indicates demand beyond short-term single-occupant rentals; it points to medium- to long-term owner-occupier and upgrade demand. This demographic structure provides a more sustainable underpinning for apartment prices.

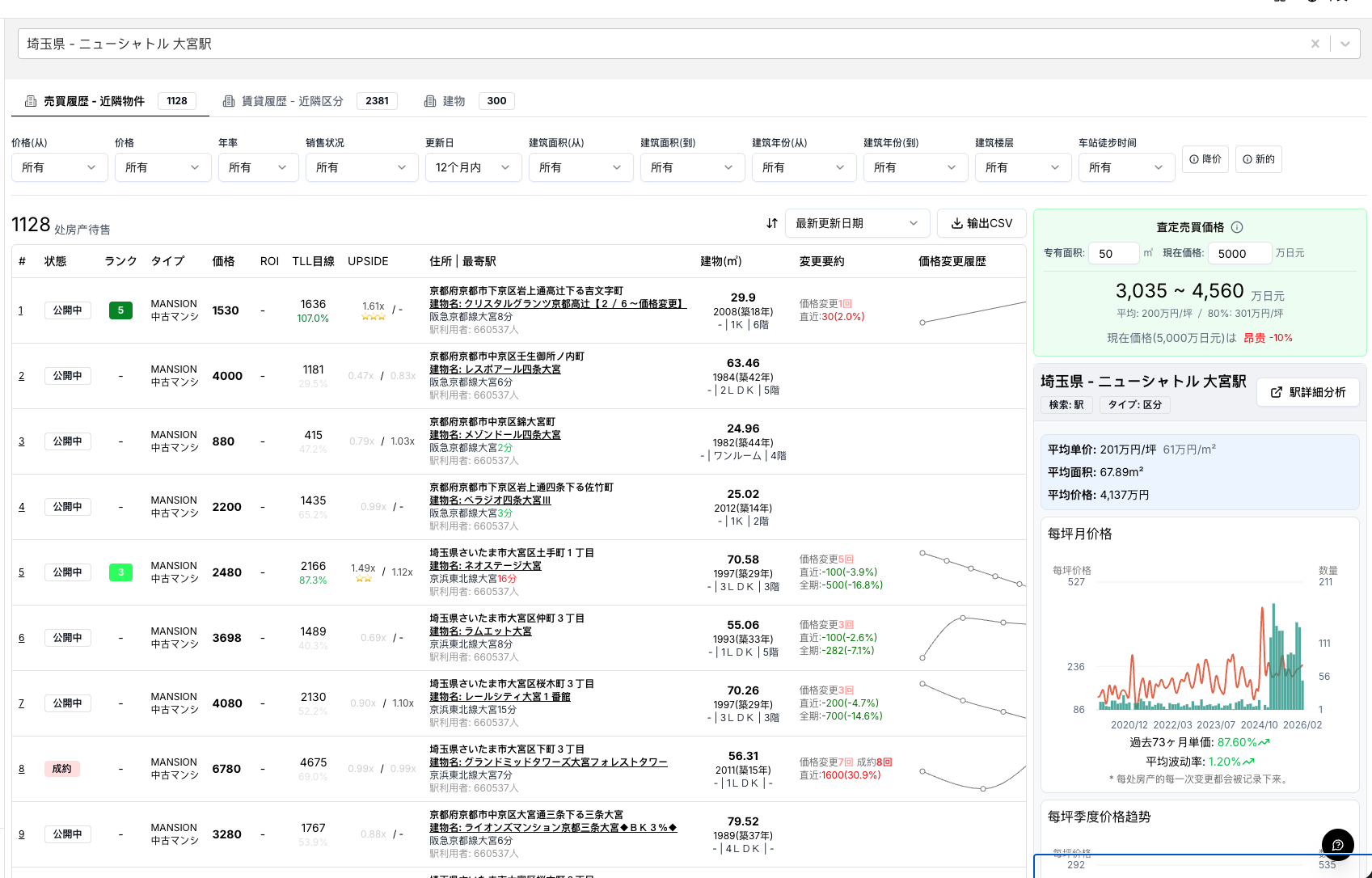

Second, transaction data and unit prices show a steady upward trend. Between 2020 and 2026 the average per-tsubo price of existing apartments around Omiya Station has risen continuously.

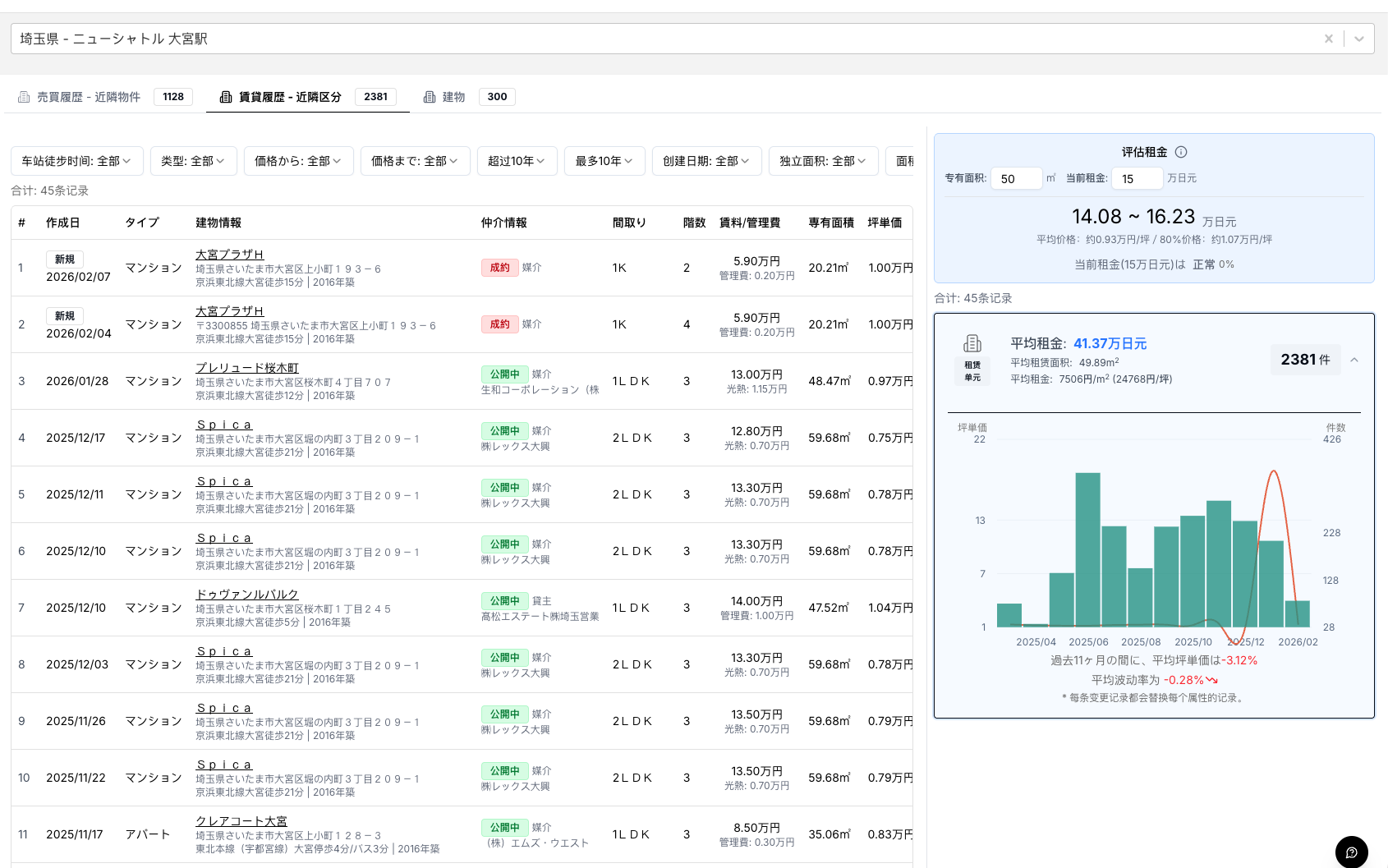

The rental market further validates this structural logic. Transit-node cities have a natural counter-cyclical quality. As an eastern Japan rail hub, Omiya’s rental demand is diverse. Tokyo commuters, young in-migrants to the metro area for work, and professionals who rely on the Shinkansen for business trips together form a multi-source rental base. Urbalytics data show long-term low vacancy rates in the area and rental adjustment cycles that are shorter than those of outlying cities. This “multi-origin demand structure” makes Omiya more resilient amid macro fluctuations.

Overall, Omiya’s recent price increases are not primarily driven by speculative capital but by a combination of demographic shifts, price mismatches and functional strengthening. Supply and demand are being re-matched, and market recognition of its “sub-center” role is steadily deepening. As the Tokyo metro enters a phase of structural differentiation, Omiya’s trajectory represents a fundamentals-driven value recovery rather than an emotion-driven spike.

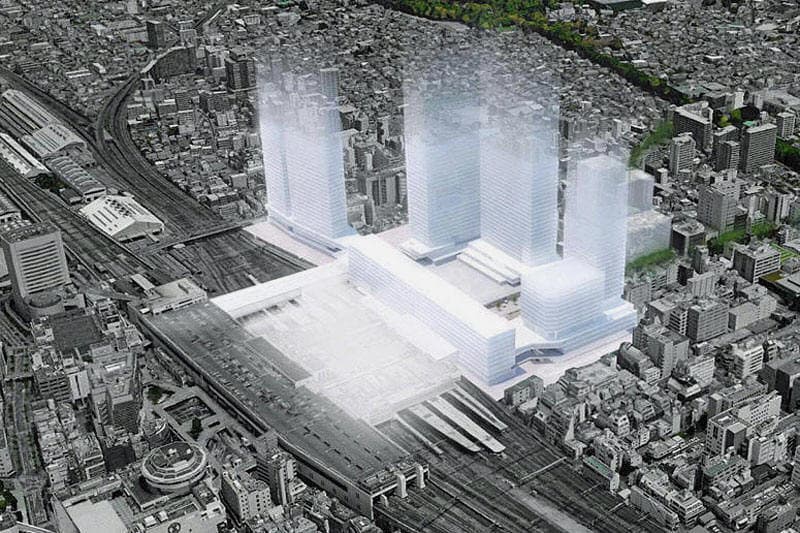

Omiya Station Redevelopment and Hub Enhancement

What truly changes market expectations is the acceleration of redevelopment.

According to Saitama City and related development announcements, several area-wide reorganization plans are underway around Omiya Station, including:

East exit area reorganization around Omiya Station

Construction of a new office-commercial mixed-use complex

Optimization of pedestrian and public spaces

Improvements to wide-area transport connectivity

The “Omiya Station Grand Central Station concept” is viewed as the core upgrade framework, aiming to raise Omiya’s urban profile as the gateway to eastern Japan. Unlike Urawa, Omiya’s strength lies not in an education brand but in the overlay of transport hub and commercial/business functions. Urawa, by contrast, has a long-established identity as a high-quality residential and educational district.

4. Logic of Asset Revaluation: Why “North of the Arakawa” Is No Longer a Discounted Zone

Past market consensus held that areas “north of the Arakawa” inherently traded at a discount. That discount stemmed from psychological distance and historical supply patterns.

However, the discount logic collapses when the following three conditions are simultaneously met:

Commuting time is controllable (30–40 minute range)

Urban functions are complete internally (not dependent on Tokyo for daily consumption)

Clear expectations of sustained redevelopment

Omiya satisfies all three conditions.

At the same time, compared with the inner Yamanote areas that have entered a global-capital pricing phase, Omiya remains in a stage dominated by domestic capital with prices not yet fully internationalized. This implies relatively controllable volatility risk while retaining upward elasticity.

Because Omiya’s demand is still primarily domestic, this means:

There remains room for price elasticity

The risk of excessive financialization is lower

External capital volatility has limited impact

Concurrently, the Tokyo metro is exhibiting a clear bipolarization: the core continues to rise while low-demand peripheral areas stagnate or decline. Omiya sits between these poles as a “structural growth belt.”

Under the current capital spillover, Omiya is no longer a mere “alternative”; it has become an independent asset class. Urawa, meanwhile, provides high-quality residential demand support along the northern axis.

As the “Route 16 myth” fades, a new value standard has emerged — not defined by geographic boundaries but by functional intensity and demand density.

References

Source: THE GOLD ONLINE, 2025, https://gentosha-go.com

Source: JR East, 2024, https://www.jreast.co.jp

Source: Saitama City official website, 2023–2024, https://www.city.saitama.jp

Source: Saitama Prefectural Board of Education, 2023, https://www.pref.saitama.lg.jp

#OmiyaInvestment #UrawaRealEstate #TokyoMetroRedevelopment #SaitamaProperty #TokyoSpilloverEffect #ShinkansenHub #OmiyaStationRedevelopment #ApartmentInvestment #JapanRealEstate #AssetAllocationJapan #SubcenterCity #TransitOrientedDevelopment #UrbalyticsAnalysis #JapanCondoMarket