Words: 1296 | Estimated Reading Time: 7 minutes | Views: 6264

After the surprising outcome of the Liberal Democratic Party leadership election, markets reacted quickly, producing a clear divergence across equities, bonds and FX: equities were supported by expectations of “stimulative fiscal policy + accommodative monetary policy,” while ultra-long government bonds and the yen came under pressure. For investors, this is not merely a macro market move; it also highlights a vulnerability in the interaction between Japan’s fiscal and financial institutions.

Immediate market reaction: the emergence of the “Takaichi trade”

With LDP leader Sanae Takaichi signaling a policy orientation that continues Abe-style fiscal stimulus, markets interpreted this as a signal that fiscal expansion and monetary easing could persist in parallel. On Monday (10/6) Tokyo stocks rallied sharply: the Nikkei 225 closed up ¥2,175 at 47,944, and TOPIX rose 96.89 points to 3,226 — both marking new record highs. Expectations that she would pursue fiscal expansion and economic stimulus intensified buying, driving a broad-based market rebound. Tokyo stocks climbed modestly again on the 7th, with the Nikkei rising for the fourth consecutive session and closing up ¥6 at 47,950, slightly extending its record closing high and setting intra-day highs together with TOPIX.

The equity move has been labeled the “Takaichi trade,” with the Nikkei touching historic levels, notably benefiting sectors tied to external demand and high-tech areas such as semiconductors and data centers. At the same time, market expectations for further Bank of Japan normalization (rate hikes) were weakened, providing near-term support to real estate sectors; however, if fiscal expansion increases government bond issuance or raises doubts about fiscal sustainability, ultra-long bond yields could rise, creating the risk of higher real estate financing costs.

Because rate hikes by the BOJ are expected to be gradual, real estate indices have outpaced other sectors.

Although this rally has been strong, the institutional risks behind it cannot be ignored. The intensity of the market response stems from Japan’s long-standing, fragile equilibrium of “fiscal expansion + BOJ unconventional policy.”

Main policy thrusts under Takaichi and potential effects on foreign nationals policy

Sanae Takaichi prioritizes a “strong nation” and “national security” agenda, placing defense, economic sovereignty and diplomatic independence at the center of her platform. Under this framework, her approach to foreigners and immigration is likely to favor strict, conditional management rather than outright exclusion. Nevertheless, her policy stance and public remarks could increase uncertainty for foreign residents in Japan, Chinese communities, multinational operators and international investors.

Her stated policy priorities include:

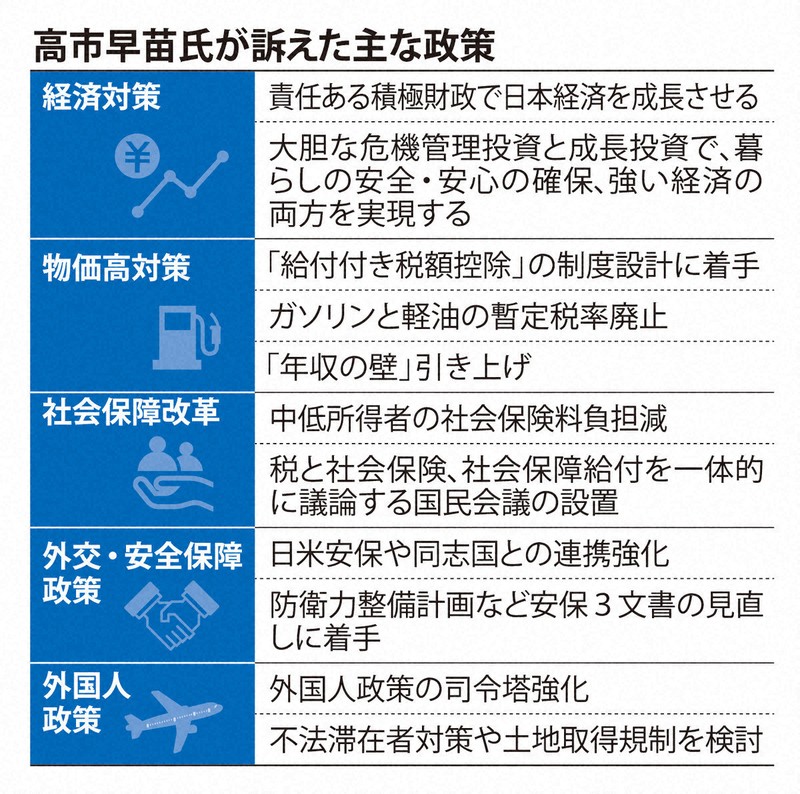

Economic policy: Measures to address inflation such as abolishing the temporary gasoline tax rate and introducing tax credits with accompanying subsidies, combined with “responsible proactive fiscal policy” to drive growth.

Security policy: Increased defense spending, establishment of cyber defenses and strengthened economic security measures to safeguard national sovereignty and security.

Science, technology and digital policy: Accelerated growth investment in cutting-edge fields such as AI, semiconductors and quantum technologies to foster innovation.

Foreign nationals policy: Strict controls on illegal overstays and foreign land purchases to address public security concerns.

Other policies: Expanded measures to address low birth rates, regional revitalization, education reform, and a shift away from “work-life balance” rhetoric toward a culture of full commitment to work.

Direction of foreign nationals policy

Based on Takaichi’s statements and media reports, her approach to foreign nationals may include the following specific directions:

Restricting foreign land purchases: Tighter limits on land acquisitions by foreigners, especially in areas deemed sensitive for national security. On October 6 the Ministry of Land, Infrastructure, Transport and Tourism revised implementation rules for the Land Use Planning Act to add nationality to the reporting items for large land transactions (such as purchase amount, intended use, owner address), seen as preparatory steps for further controls.

Stricter enforcement on illegal residence: Increased enforcement actions against overstayers and tougher measures, potentially including more enforcement personnel to ensure strict compliance.

Reconsideration of immigration policy: A willingness to rethink foreign policy from the ground up, especially regarding groups with significant cultural and background differences.

Revision of the Technical Intern Training Program: Although a decision was made in June to replace it with a new Development-to-Employment scheme, Takaichi’s stance may influence future implementation details, with greater emphasis on skills training and repatriation.

Takaichi’s direction on foreign-national policy could have multiple impacts. On one hand, stricter enforcement and tighter controls could make some communities feel that public safety has improved, particularly in areas concerned about the security implications of foreign populations. On the other hand, tighter restrictions on foreign labor could exacerbate labor shortages in construction, nursing and agriculture — sectors that rely heavily on foreign workers to fill vacancies. Although she emphasizes stimulating domestic growth, a reduction in foreign labor could dampen economic activity for businesses that depend on foreign employees. Thus, while residents may perceive stronger social control, Japan’s economy could face challenges from reduced labor supply.

Institutional vulnerabilities: investor risks and opportunities

To place this market volatility into an institutional context, the key is Japan’s long-standing combination of “fiscal dependence + central bank unconventional policy.” Government debt-to-GDP has been high for an extended period, and fiscal policy is easily instrumentalized during political cycles to deliver short-term stimulus. Simultaneously, the BOJ has shouldered the task of depressing long-term rates under negative rates and yield curve control (YCC). This implicit fiscal-monetary cooperation can suppress default risk in calm periods, but when political direction shifts significantly (for example, if Takaichi advocates more aggressive deficit financing for defense or tax cuts), markets will quickly reprice bond supply and monetary policy boundaries, amplifying effects on interest rates and the currency.

Institutional shortcomings mainly appear in three areas:

Weak fiscal rules: Current laws and budgetary procedures lack effective checks against rapid fiscal expansion, increasing the policy discretion over debt issuance.

Central bank independence: Market confidence in BOJ independence can be questioned under political pressure, particularly if the government signals that deficit financing is a policy tool; markets may then suspect forced monetization, altering term premia.

Lagging disclosure and risk measurement: Especially in real estate, local government liabilities, land disposals and tax incentives are fragmented and delayed, making it difficult for market models to absorb data quickly and causing valuation errors when political conditions change.

Translating these institutional insights into investment practice yields multi-layered impacts. In the short term, if markets believe fiscal expansion will coincide with low rates, real estate equities, REITs and highly leveraged developers may receive valuation premiums; assets with stable cash flows and lower interest-sensitivity — such as logistics real estate, data centers and certain residential projects — could attract capital. However, this positive narrative masks the medium- to long-term risk of an interest-rate regime shift: if fiscal expansion prompts concern over government bond supply, investors may demand higher term premia, pushing ultra-long yields up, which raises refinancing costs, compresses developer margins and increases loan default probability. Japanese real estate is particularly sensitive to rising rates given widespread use of long-term floating or repricing debt structures.

Conclusion: from short-term market moves to long-term resilience

Takaichi’s ascent is not a simple, one-sided positive — it represents an institutional stress test.

Short-term policy stimulus can lift equity and real estate valuations, but fiscal sustainability, BOJ independence and foreign capital regulation interacting over the medium term will determine market direction.

In this environment, real estate investment success will no longer hinge on “calling the market,” but on the ability to build sufficient investment resilience using data and risk models.

References

[Source: Asahi — Mandatory nationality reporting for large land acquirers; MLIT to better track foreign transactions, 2025 (original report)] https://news.yahoo.co.jp/articles/6bc0a3c38235915901a6fff615a76851f116f415

[Source: Mainichi — What does Takaichi’s “responsible proactive fiscal policy” mean? Concerns about fiscal deterioration, 2025 (original report)] https://mainichi.jp/articles/20251004/k00/00m/010/247000c

[Source: Yomiuri — Prominent hawk Takaichi criticized for comments on foreigners during the leadership race… experts say “leader’s remarks require greater caution,” 2025] https://www.yomiuri.co.jp/politics/20251005-OYT1T50052/