![[Case 04] Income Building on Yokohama Streetfront|Resold Threefold After Three Months?](/_next/image?url=https%3A%2F%2Fs3.ap-northeast-1.amazonaws.com%2Furbalytics.reins.downloads%2Fblog-images%2F1763600994323-Screenshot%202025-11-20%20at%2010.09.43.png&w=3840&q=75)

Words: 1754 | Estimated Reading Time: 9 minutes | Views: 3339

Since Urbalytics launched, we've received many user comments: “Feature-rich, but don’t know where to start.”

This article presents a property that was resold at roughly three times its previous price and shows how to use Urbalytics to make more rational investment decisions.

⚠️ Note: Some features (such as rent lookup) are paid features and are available only to paying users.

#1 Property Information

Basic Information

Listing link: https://www.urbalytics.jp/ex/search/cm99rro8k000jl404uz0l2xde

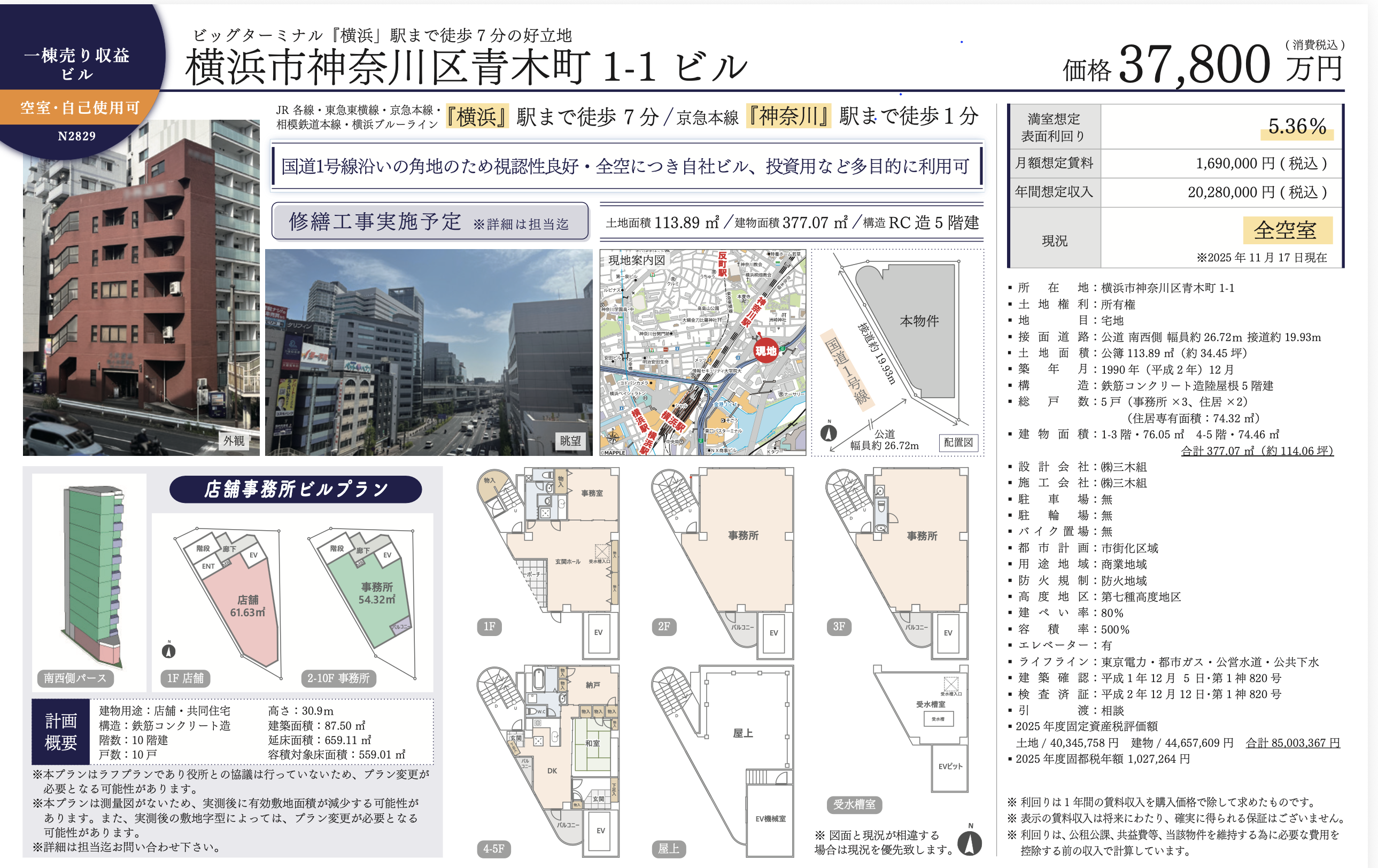

This entire income-producing building is located at 1-1 Aokicho, Kanagawa-ku, Yokohama, approximately a 7-minute walk to JR "Yokohama" Station and 5 minutes to Keikyu "Kanagawa" Station. It occupies a prime “central Yokohama × within walking distance of the station” location. The building is a 5-story RC structure above ground with a land area of 113.89 m² and a total floor area of about 377 m². It faces National Route 1 on a corner lot with high visibility, suitable for offices, clinics, or a mixed owner-occupier/investment use.

The property is currently completely vacant, but the seller estimates full occupancy annual income at about ¥20,280,000, corresponding to a gross yield of 5.36%. The 1st floor is roughly 61 m² retail space; floors 2–5 are configured as offices, and some floors include rooftop terraces. Given the stable demand around Yokohama Station, the building’s modern facade and regular floor plates, this asset may appeal to SMEs, owner-occupiers, or investors planning a full renovation. Note that the listing indicates "repair works planned", suggesting potential exterior or equipment upgrades and possible additional costs; additionally, the building was completed in 1989 and, although it meets newer seismic standards, buyers should further verify major systems such as elevators, fire protection, and plumbing.

Urbalytics Overall Property Analysis

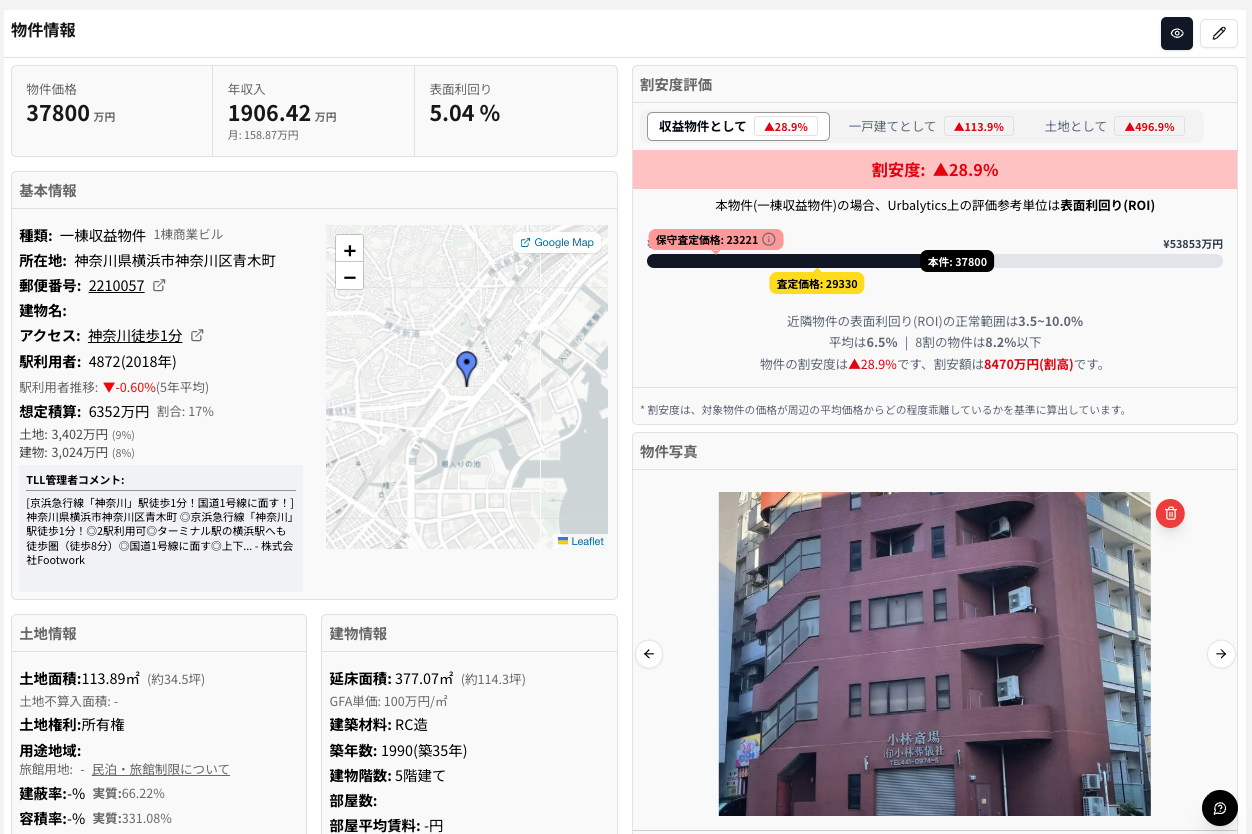

Urbalytics’ valuation indicates that the property’s discount/overpricing metric is -28.9%, meaning its price is more than roughly 30% higher compared with comparable income properties in the area.

Based on the current asking price of ¥378,000,000, the system estimates:

Conservative appraised price of approximately ¥232,210,000,

Estimated reasonable price of approximately ¥293,300,000, which implies a potential negotiation gap of about ¥84,700,000.

By area comparison, similar income properties’ typical gross yield (ROI) ranges from 3.5% to 10.06%, averaging about 6.5%. This property’s ROI is 5.04%, clearly below the market average, indicating it is priced high with a relatively low yield and therefore appears overvalued among income assets.

❌ Caution — Rents Appear Significantly High

"Rent Upside" typically indicates room for rental increases, but here it is negative (-41.7%), which means there is not only no upward room but rents are already high. The rent level may already be at market peak, and if tenants vacate, re-letting may require lowering rents to maintain occupancy. Although the location is advantageous—close to Yokohama and a corner site with excellent visibility, suitable for retail leases—this type of income asset can be costly to lease for typical owners and requires extreme caution.

For investors, this implies:

Current cash flow may be high, giving attractive short-term returns;

but there is a material risk of rental correction going forward, so long-term sustainability must be evaluated.

Given the building is currently fully vacant, the seller has a high probability of overstating projected rents to inflate the asking price.

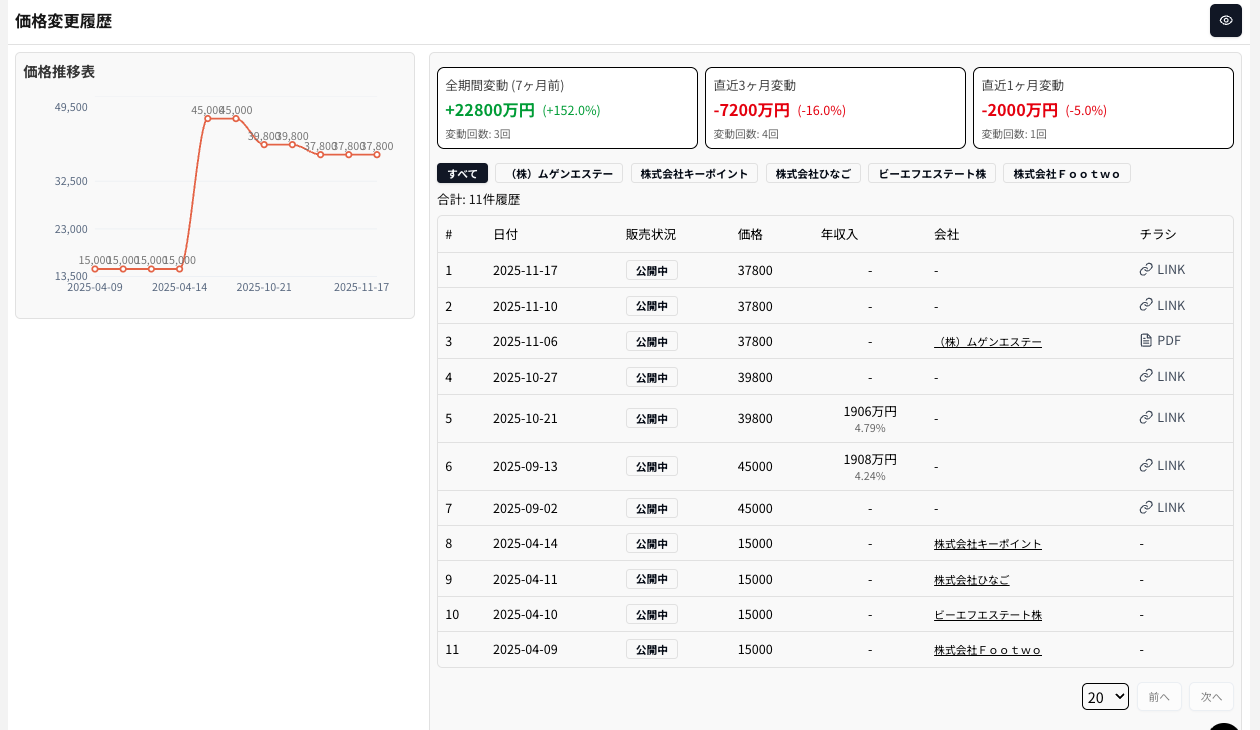

#2 Price Reduction History

According to Urbalytics’ price records and market transaction data, this property shows an unusually volatile price trajectory. The property was sold around April 2025 for about ¥150,000,000, then immediately re-listed at a substantially higher asking price of approximately ¥450,000,000, a rise of +200% (roughly 3x), which is a rare and extreme markup on relisting. The price was then slightly adjusted a month later to test the market.

Notably, Urbalytics’ reasonable valuation is only about ¥293,000,000, showing a large gap to the seller’s relisting price and indicating that the asking price lacks fundamental support.

The pattern of "contract → large multiple markup → relist" is typical of a flipped asset. Such cases usually carry the following risks:

Price deviates excessively from the market: the seller’s asking price is up to three times the previous contract price, far outside acceptable ranges for the area and comparable income properties.

Gross yields become unreasonable: the high price compresses ROI to around 5%, making it unattractive relative to the area average (~6.5%).

High liquidity risk on exit: even if purchased, it may be difficult to find buyers willing to accept the same premium later.

Large theoretical negotiation room but practical difficulty in closing — if the seller insists on the high price, the property may remain on the market for a long time; if the seller is willing to negotiate, the buyer has strong leverage, using the prior contract price (~¥150,000,000) and Urbalytics’ reasonable price (~¥293,000,000) as anchors.

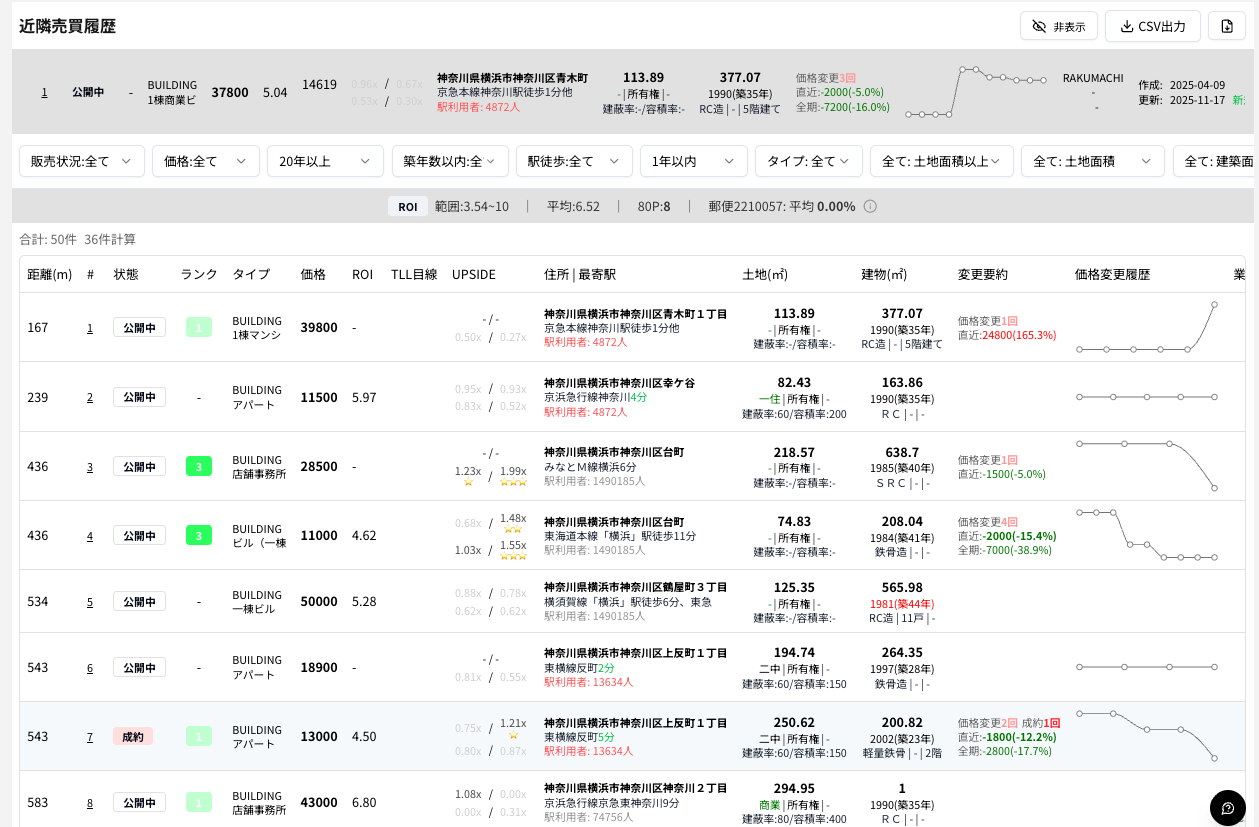

#3 Nearby Prices

Urbalytics’ "Nearby Sales History" shows this property (Aokicho, Kanagawa-ku, Yokohama, asking ¥378,000,000) located north of Yokohama Station in a mature mixed commercial-residential zone. Within a 1 km radius there are roughly 50 comparable properties. The local price band is wide, ranging from about ¥11,000,000 to ¥500,000,000; properties similar to this case (whole-building commercial/office use, RC structure, floor area 200–400 m²) are mostly listed in the ¥100,000,000–¥150,000,000 range, which is clearly below this property’s asking level.

In terms of income performance, the area average ROI is approximately 6.5%, with the 80th percentile at 8.2%, representing a relatively healthy yield band for central Yokohama. This property’s gross ROI is only 5.04%, ranking below most comparable assets locally and showing weaker income characteristics. Urbalytics’ TLL target line also indicates this property underperforms the expected average and lacks investment appeal relative to nearby options.

4 Rent Analysis

Urbalytics’ "Rent Upside" data shows the property’s current rent level is significantly higher than comparable nearby properties, exhibiting the characteristic of a "high-rent" asset.

First, using nearby sales comparables as reference, this property’s average rent is 41.0% above the area average; compared with nearby rental transaction comparables for whole-building leases, it is still 44.2% higher, indicating overall rents are well above market. The only positive signal appears when comparing on a subdivided (unit-by-unit) lease basis, where this property looks relatively lower versus large-area subdivided cases, but that comparison has limited relevance for whole-building investments.

Looking at the rent structure, the 39 local comparables are mostly RC or apartment-style income buildings from the 1980s–1990s, with monthly rents generally in the range of ¥5,000–¥11,000 per m². This property’s current effective rent is well above that band, which indicates the landlord has adopted an aggressive rent strategy. Given this is an "older building + large area" combination, the high rent is particularly anomalous and may reflect:

Artificially elevated rents set by agents to support nominal yields;

tenants with special uses (e.g., offices, storage) accepting rents above residential rates;

value-add premium following recent full-building renovations or improvements;

or differences in how leaseable area is calculated that produce nominally high rents.

Overall, this property is classified in the market as a "high-rent type" income asset, and its income is highly sensitive to rent levels. Investors should pay particular attention to:

Whether the current rent levels are sustainable

Whether lease terms contain early termination risks

Whether the market would accept the same rent level on exit

If rents revert to the area average, the potential NOI decline is material and should not be ignored.

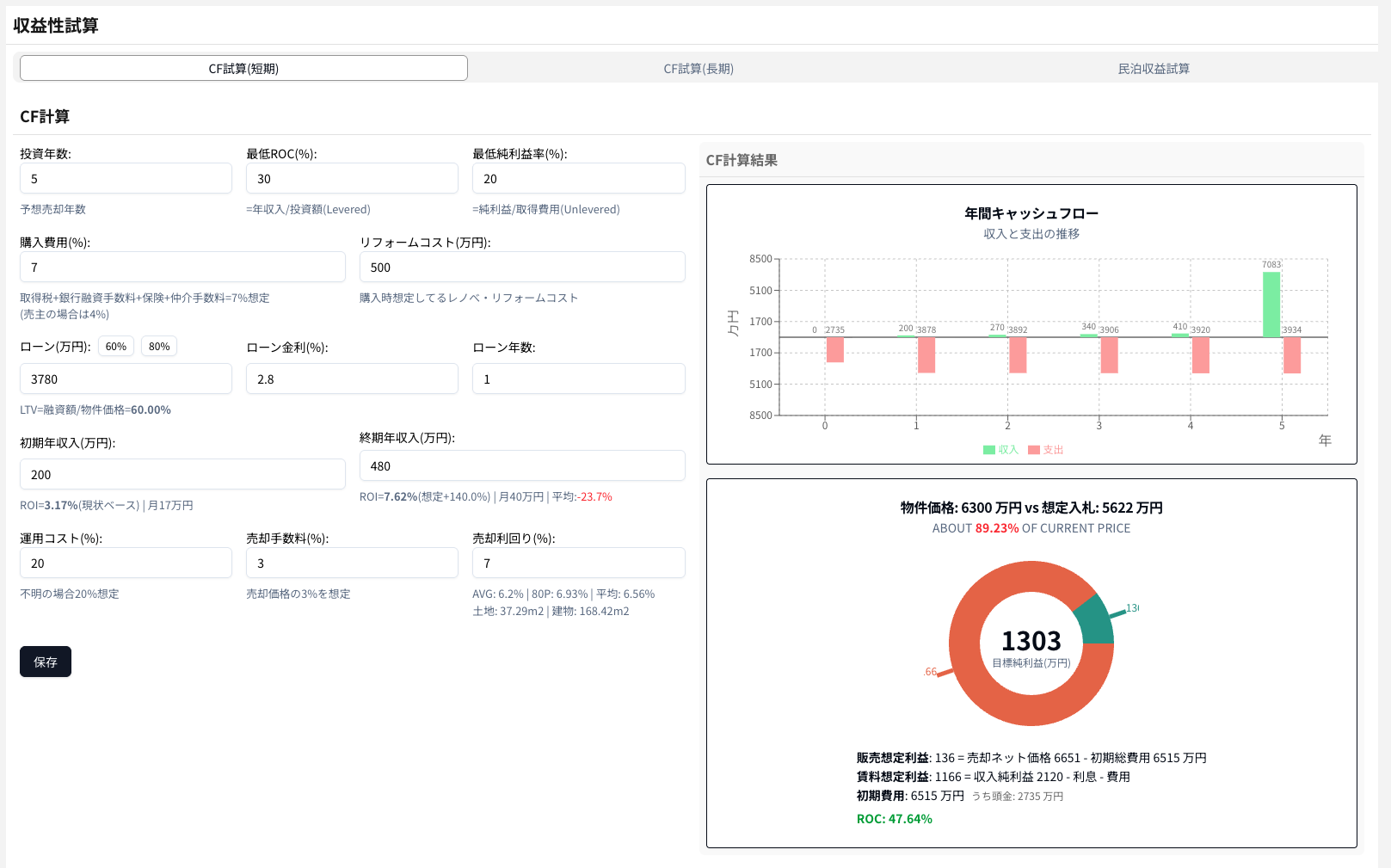

5 Overall Investment Yield Analysis

This Urbalytics cash-flow simulation is based on a one-year hold quick-investment model. Assumptions: loan-to-value of 40% (loan ¥12,000,000), interest rate 2.8%, term 1 year. Purchase costs are estimated at 4% of the purchase price, with no additional renovation costs. Operating expenses use an industry standard rate of 20%, and the sales commission is 3%.

Rent is assumed flat (no growth), with beginning and ending annual income both at ¥19,080,000, keeping the gross yield at 5.04%. On the sale side, a conservative 6.5% exit capitalization rate is used to estimate terminal value, which is a cautious approach to avoid overstating future returns.

The chart to the right shows annual cash-flow movements: in year one, because of purchase fees and financing costs, there is an approximate ¥137,000,000 cash outflow; in the sale year, asset disposition produces about ¥126,000,000 net inflow, bringing the total cash flow back to positive. The pie chart shows the total target profit of ¥38,690,000, composed of ¥11,900,000 rental net income and ¥26,780,000 sale net income, yielding an overall ROC of approximately 28.05%, which is a strong result for a one-year project.

More importantly, the model’s reasonable "indicative bid" is approximately ¥248,000,000, about 65.6% of the current asking price of ¥378,000,000, a very large discrepancy that implies purchasing at the current price would make it difficult to reach the model’s target returns.

From an IRR perspective, to achieve a target IRR of 20% or more under the current rent and sale assumptions, the acceptable bid should be around ¥250,000,000 (roughly 65%–66% of the asking price).

Considering the property was previously sold at a low price and then relisted at a much higher price by a reseller, achieving such a discount in the short term is highly unlikely. If interested, we recommend waiting and monitoring the market.

Conclusion

This whole-building income property in Aokicho, Kanagawa-ku (a 1-minute walk to Kanagawa Station) is currently listed at ¥378,000,000. Urbalytics indicates the property is priced approximately 28.9% above the area’s reasonable price, with a gross yield of 5.04%, slightly below the average yield of nearby properties. Although the asset benefits from frontage on National Route 1, corner-site visibility, and mixed retail/office usage, the building was completed in 1990, shows signs of aging and multiple areas needing repair, and is currently fully vacant—meaning rent recovery will take time. Model estimates suggest a prudent bid to meet target ROC and yields would be around ¥248,000,000 or lower (about 65% of the current price), indicating the current asking price contains a clear premium. Given the property’s history of a low-price sale followed by aggressive relisting, evaluate the cash-flow recovery timeline, vacancy risk, and reliance on exit pricing with caution. Investors should be careful and avoid entering a flipped asset at an excessively high cost.

Property link https://www.urbalytics.jp/ex/search/cm99rro8k000jl404uz0l2xde

If you want a similar analysis for your own property, sign up for a free trial of Urbalytics:

👉 https://urbalytics.jp/login?tab=signUp

Or send us your property details and we will prepare a customized report for you 📩