![[Case 02] Takada 3-chome, Toshima Ward | Entire Income Building Resold at JPY 220,000,000 — A Twofold Resale Flip](/_next/image?url=https%3A%2F%2Fs3.ap-northeast-1.amazonaws.com%2Furbalytics.reins.downloads%2Fblog-images%2F1762146957221-Screenshot%202025-11-03%20at%2014.00.15.png&w=3840&q=75)

Words: 1613 | Estimated Reading Time: 9 minutes | Views: 2716

Since Urbalytics launched, we have received a lot of user feedback: “Feature-rich, but don’t know where to start.”

This article walks through a real investment property case to show how to use Urbalytics to make investment decisions.

⚠️ Note: Some features (such as rent lookup) are paid features and are available only to paying users.

#1 Property Information

Basic Information

Property link: https://www.urbalytics.jp/ad/blog/edit/cmhbpttct0005ld04a01no9kl

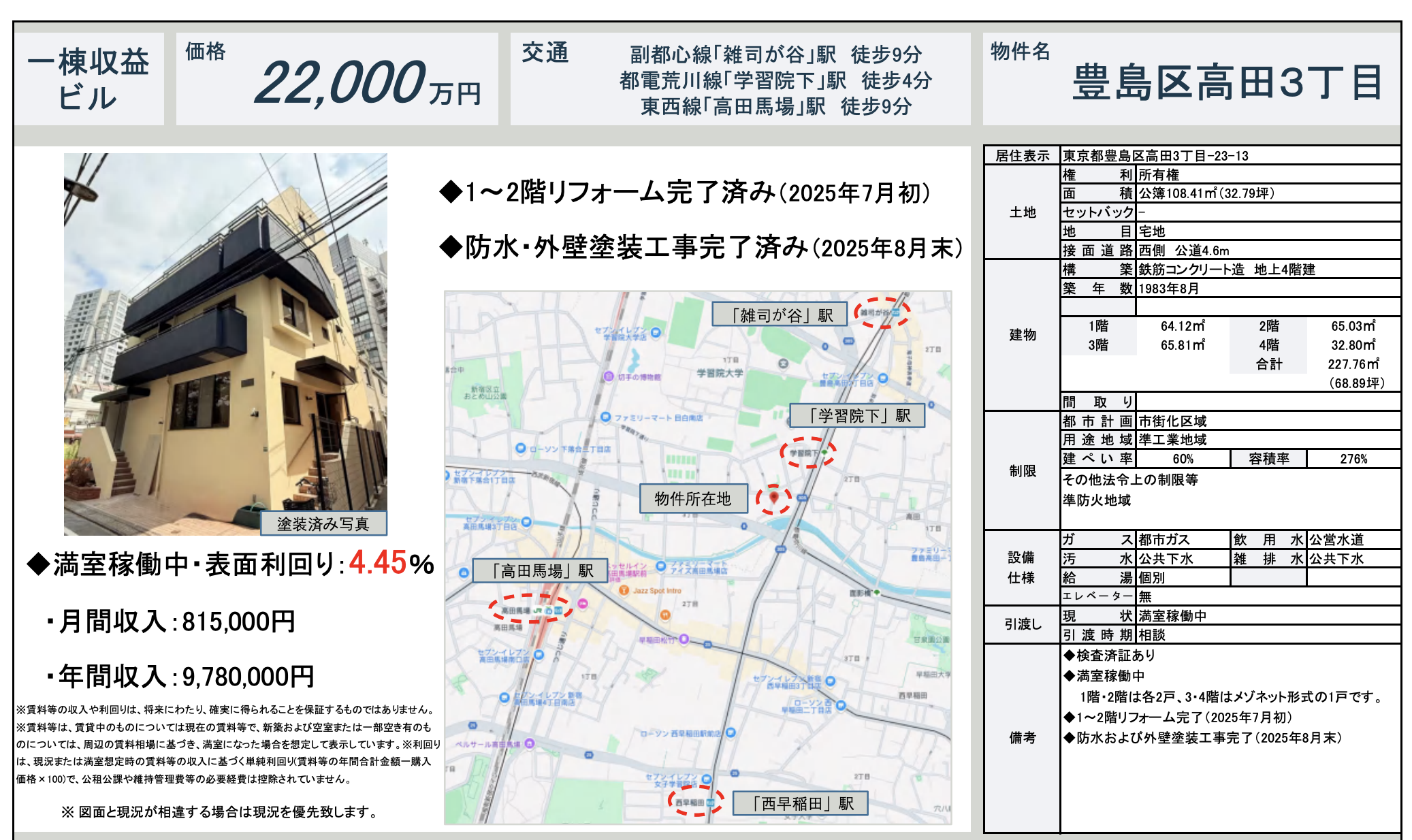

This income-producing building is located in Takada 3-chome, Toshima Ward, Tokyo. It is about a 9-minute walk to the Fukutoshin Line Zoshigaya station (雑司が谷), a 4-minute walk to the Toden Arakawa Line Gakushuinshita station (学習院下), and a 9-minute walk to the Tozai/Seibu lines at Takadanobaba station (高田馬場), offering convenient transport access. It sits near the university and residential districts around Waseda and Takadanobaba, with well-developed local amenities.

The building was completed in August 1983, is reinforced concrete (RC), has four above-ground floors, a total floor area of approximately 227.76 m² (68.89 tsubo), and a land area of approximately 108.41 m² (32.79 tsubo). The property has undergone waterproofing and exterior painting (August 2025), and interior renovations for floors 1–2 are expected to be completed in July 2025. The building is currently fully occupied, with monthly rental income of JPY 815,000, annual income of approximately JPY 9,780,000, corresponding to a gross yield of 4.45%.

Notably, the property is close to an area popular with Chinese investors — Takadanobaba. Takadanobaba is a typical student district: the area hosts multiple universities, vocational schools, and cram schools, and the resident profile is dominated by students and young single occupants. In particular, many Chinese-run cram schools have opened recently, attracting significant investor interest.

Urbalytics Overall Property Analysis

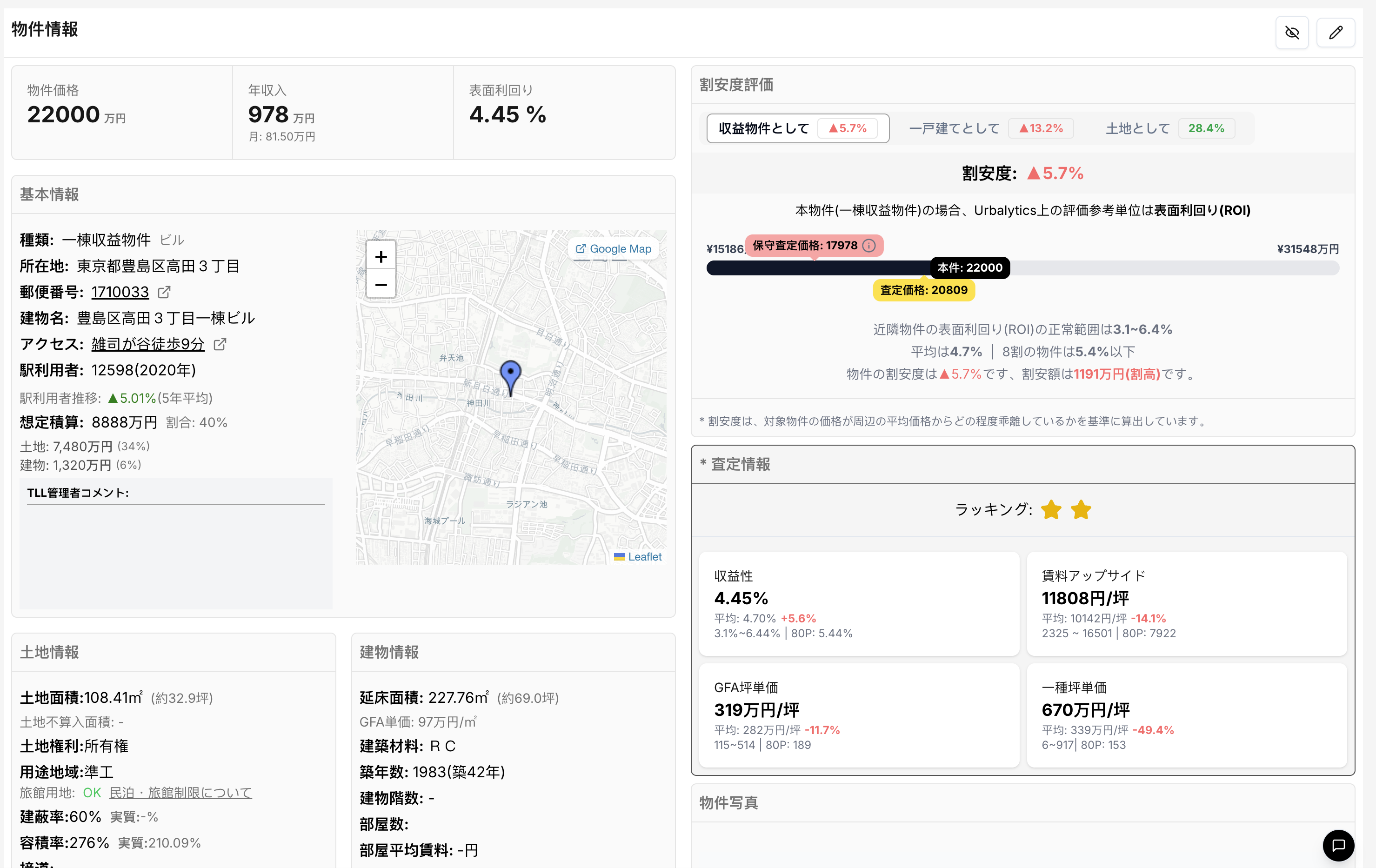

Urbalytics’ valuation indicates that, as an income property, this building’s price gap is -5.7% — in other words, its listing price is slightly above the market’s reasonable range for comparable properties. At the current listing price of JPY 220,000,000, the system estimates:

Conservative assessed price: approximately JPY 179,780,000;

Estimated fair price: approximately JPY 208,090,000;

The property is priced about JPY 11,910,000 above the market benchmark.

On yield, comparable whole-building income properties in the area typically show gross yields in the range of 3.1%–6.4%, averaging about 4.7%. This property’s ROI of 4.45% is slightly below the regional average, classifying it as a relatively stable, low-volatility income asset.

❌ Cautions — Slightly lower yield, limited upside for rents

Urbalytics’ rent analysis shows the “rent upside” metric at JPY 11,808 per tsubo, which is about 14.1% higher than the regional average of JPY 10,142 per tsubo. This indicates current rents are approaching the market ceiling, and short-term additional upside is limited.

From an investment perspective, while the property’s rent performance is strong, its overall yield is below the area median. If tenant turnover or a market correction occurs, maintaining rents may be challenging. In addition, the building is over 40 years old, so future capital expenditures (CapEx) such as exterior, waterproofing, and equipment replacements should be factored into projections.

Because the area is very familiar to Chinese buyers, it is understandable that the premium reflects a willingness among these buyers to pay for convenience and familiarity.

#2 Price Reduction History

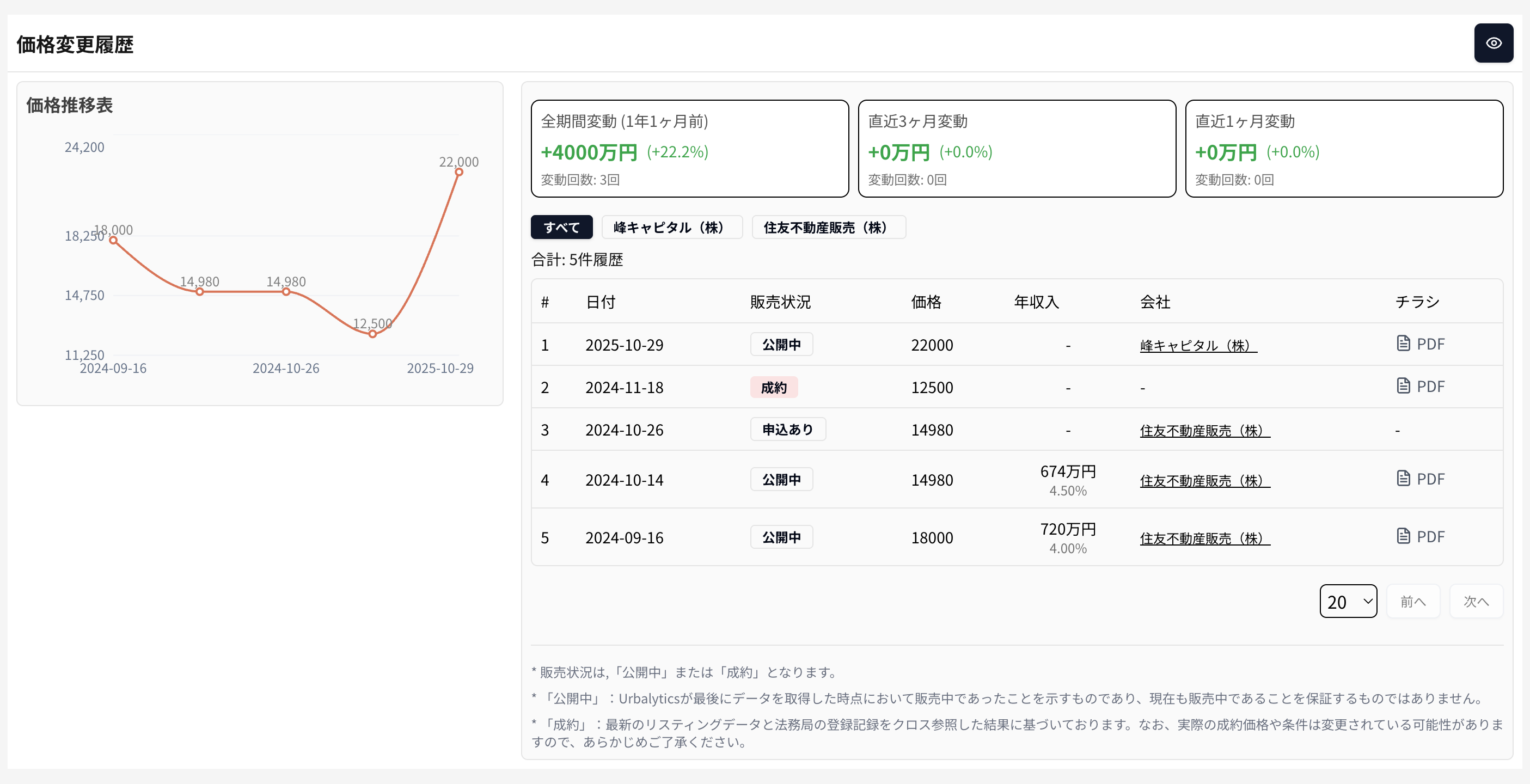

Urbalytics’ price history shows significant volatility over the past year, exhibiting a typical “short-term re-listing (re-sell)” pattern. Records indicate:

First publicly listed in September 2024 at JPY 180,000,000;

The price was subsequently reduced and reached a low of JPY 125,000,000 in early 2025;

It recorded a sale at JPY 125,000,000 in November 2024;

However, in October 2025 a new seller re-listed the property with an asking price of JPY 220,000,000, an increase of +75%, reaching a historical high.

Overall, the asset went through a typical “sell → refurbish → re-list” re-sell cycle within a short period. The cumulative price increase within the year is about +22.2%, and the current price is nearly double the last recorded sale price.

The property’s current gross yield is 4.45%, only slightly above the regional median range (4.2%–4.7%). Given the substantial price increase, effective yield has declined. When evaluating such “post-refurbishment high-price re-sell” assets, investors should pay particular attention to:

Whether the quality and scope of refurbishment justify the premium;

Whether current rents have been artificially inflated by the seller to sustain nominal yields;

Market acceptance and re-liquidity at this price level.

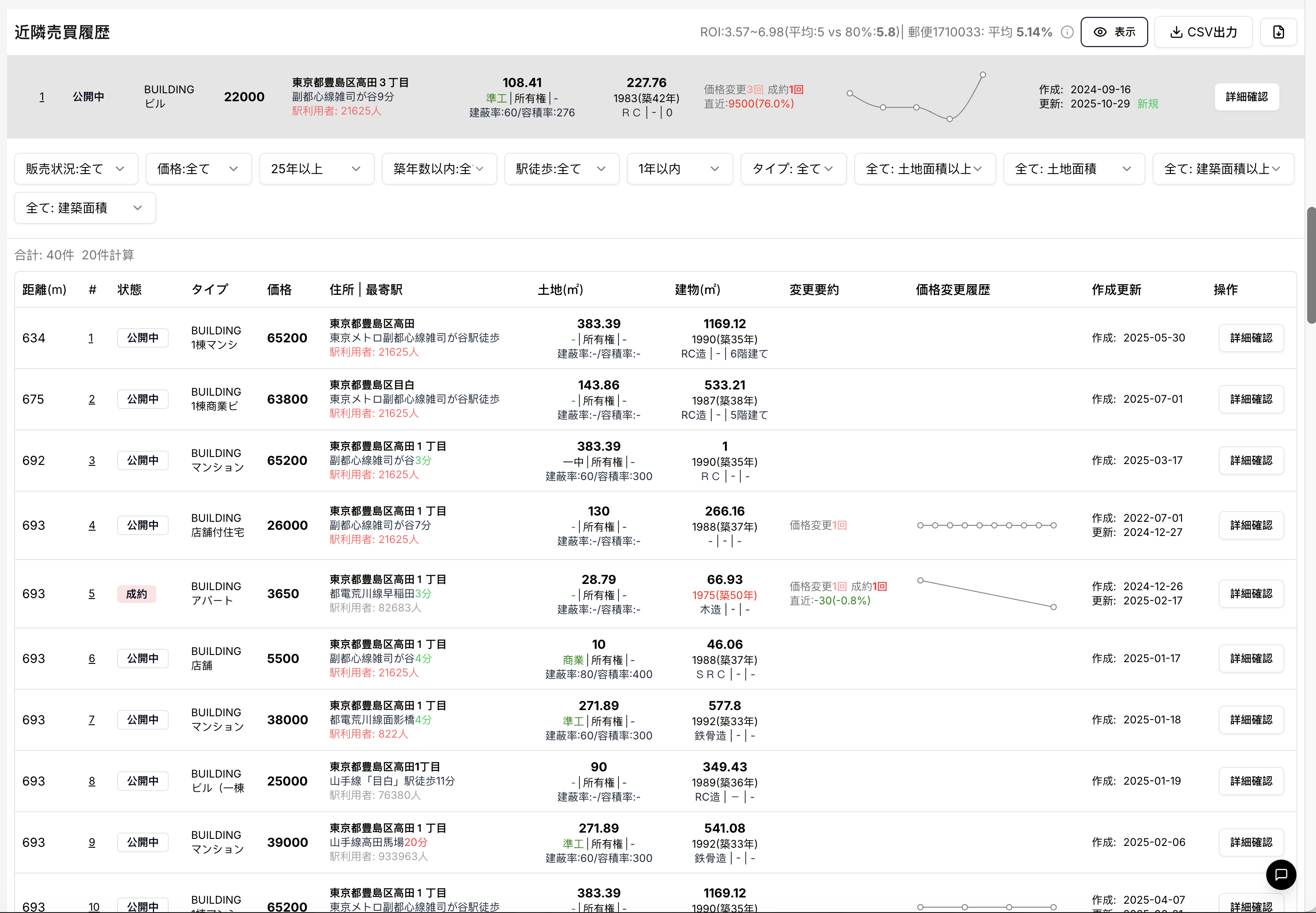

#3 Nearby Property Prices

According to Urbalytics’ “nearby sales history,” this property (Takada 3-chome, Toshima Ward; listed at JPY 220,000,000) sits in the core Takadanobaba–Zoshigaya living area and is a mature residential-and-school district within Tokyo’s 23 wards. The system shows 40 similar income properties within a 1 km radius. For properties with floor areas between 200–600 m², prices are generally distributed between JPY 20,000,000 and JPY 650,000,000, with an average gross yield of about 5.1% and an 80th percentile yield of 5.8%.

Notable trends from surrounding listings and transactions include:

Overall regional prices are consolidating at a high level: for example, several RC income buildings in the same district (e.g., properties in Takadanobaba 1-chome listed at approximately JPY 652,000,000 and JPY 638,000,000) are large-scale but show no significant increase in unit-area price, indicating market stabilization.

Small- to mid-sized properties are more active: transactions and updates are concentrated in four-story RC or wooden income buildings built in the 1980s–1990s, reflecting investor preference for renovating older buildings and targeting short-term cash-flow plays.

This property’s pricing is clearly aggressive compared with similarly sized leased assets: for example, a nearby income building of about 530 m² in Takada 1-chome is listed at approximately JPY 630,000,000, with a similar unit-area price but greater scale and leasing potential, implying this case carries a relatively high unit land and building price.

In summary, although the property benefits from a strong location and recent refurbishment, it presents characteristics of an aggressively priced, lower-yield re-sell type asset: the seller has elevated appearance and rents via short-term refurbishment and re-listed at a premium. Investors evaluating such assets should focus on rent sustainability and market absorption capacity to avoid the risk of “buying at a high price with low liquidity.”

4 Rent Analysis

Urbalytics’ “rent upside” analysis indicates this property’s current rent level is significantly higher than comparable nearby assets. System data show:

Compared with all nearby income properties, this property’s average rent per tsubo is JPY 11,800/tsubo, about 14.1% higher than the regional average;

Using whole-building income properties as the reference, this property’s rents are about 16.4% higher.

Regarding market rental structure, rents around Toshima Ward and Takadanobaba generally range between JPY 10,000 and JPY 13,000 per tsubo.

This property’s current JPY 11,800 per tsubo sits near the upper bound of that range, indicating the landlord has adopted a relatively aggressive pricing strategy, likely reflecting the premium from recent refurbishments (exterior painting and interior updates).

5 Overall Investment Yield Analysis

💼 Model Assumptions and Premises

Based on Urbalytics’ short-term cash flow model, this analysis assumes a 5-year holding period, 60% loan-to-value, loan interest rate of 2.8%, and loan term of 1 year. No additional renovation costs are assumed at purchase (reform cost = 0). Acquisition fees are estimated at 7% of the purchase price. Operating expenses are set at 20% of annual income, and the selling commission is 3%.

The model assumes no rent growth; initial and terminal annual income are both JPY 9,780,000, and the gross yield remains fixed at 4.45%. Final sale proceeds assume annual capital appreciation of 5.5%. This represents a conservative income assumption without rent increases or additional upside from further renovations.

📈 Model Results and Cash Flow Performance

The cash flow chart shows relatively stable annual cash flow for the first four years, with income and expenses nearly balanced, and a significant cash inflow in year five due to the sale. The pie chart indicates a total target profit of approximately JPY 25,190,000, of which rental net income is about JPY 20,640,000 and sale net income about JPY 4,550,000. Based on this, the ROC (Return on Cost) is approximately 70.1%, indicating a moderate-to-high capital return potential under conservative assumptions.

From a valuation perspective, the model’s suggested reasonable entry price is approximately JPY 156,950,000, which is about 71.3% of the current listing price (JPY 220,000,000).

👉 From an IRR standpoint, if an investor targets roughly a 20% internal rate of return under the above assumptions, the target offer should be around JPY 156,000,000 (approximately 70%–72% of the listing price).

Given the property was recently refurbished and the seller is a re-seller, achieving a large discount in the short term is difficult.

Summary

This whole-building income property in Takada 3-chome, Toshima Ward is currently listed at JPY 220,000,000. Urbalytics estimates the price is about 6% above the market’s reasonable range, with a gross yield of 4.45%, slightly below the regional average. The property has completed exterior and waterproofing refurbishments, and current rents are near the market ceiling, so future upside is limited. The cash flow model shows that under conservative assumptions and a 5-year hold, an investor could achieve about a 70.1% ROC. To target a 20% IRR, a reasonable entry price would be around JPY 156,000,000, roughly 70% of the listing price. Because the property was recently refurbished and is being resold by a re-seller, obtaining a deep discount in the short term is unlikely.

Property link: https://www.urbalytics.jp/ad/blog/edit/cmhbpttct0005ld04a01no9kl

If you would like a similar analysis for your own property, sign up for a free trial of Urbalytics:

👉 https://urbalytics.jp/login?tab=signUp

Or send us your property information and we will prepare a custom detailed report for you 📩