![[Case 01] JPY 63,000,000 — 10%: RC Investment Building, 3-Min Walk to Keisei-Tateishi, Katsushika](/_next/image?url=https%3A%2F%2Fs3.ap-northeast-1.amazonaws.com%2Furbalytics.reins.downloads%2Fblog-images%2F1761725288924-1.png&w=3840&q=75)

Words: 1417 | Estimated Reading Time: 8 minutes | Views: 1428

Since Urbalytics launched, we have received many users’ feedback: “Feature-rich, but don’t know where to start.”

This article uses a real investment property case to show how to make investment decisions with Urbalytics.

⚠️ Note: Some features (such as rent lookups) are paid features and are available only to paid subscribers.

#1 Property Information

Basic Information

Listing link: https://urbalytics.jp/ex/search/cmd4jvjjr0005pxwkipx5iz1w

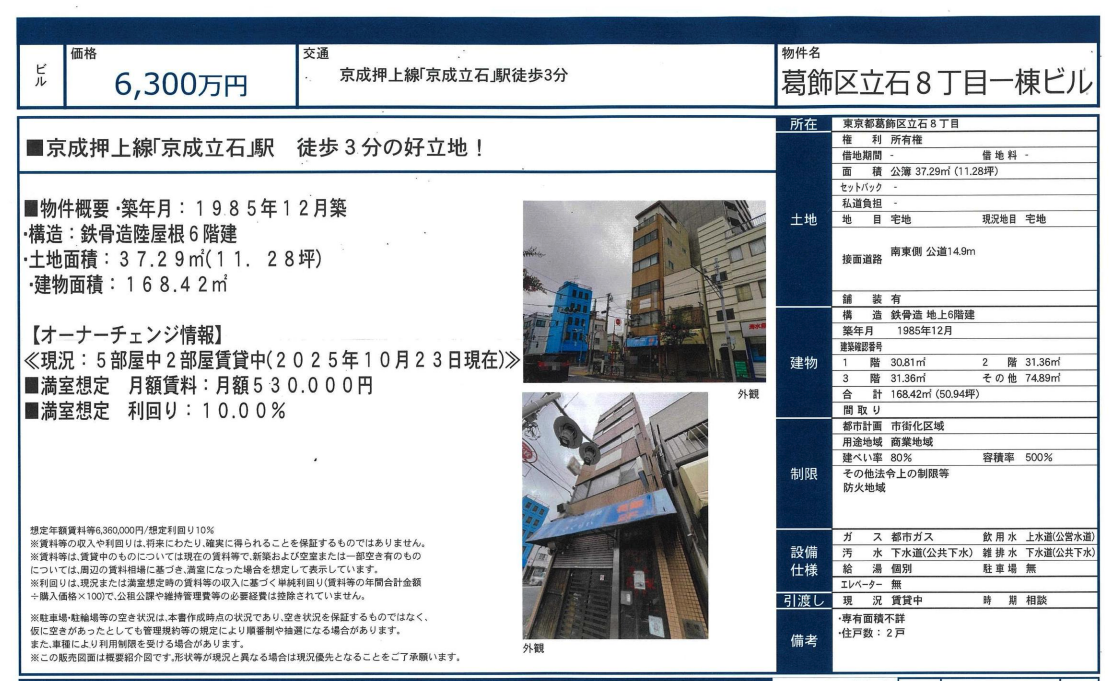

This entire income-producing building is located in Tateishi 8-chome, Katsushika-ku, Tokyo, a three-minute walk from the Keisei Line "Keisei-Tateishi" station. The location is excellent, in a mature mixed commercial-residential area.

The building was completed in December 1985. It has a steel-frame structure, six above-ground floors, a total building area of approximately 168.42 m², and a land area of about 11.28 tsubo. Although the land parcel is small, the building utilization is high. The site faces a southeast road approximately 14.9 m wide, offering good daylighting and visibility, suitable for small offices, retail, or professional uses.

Currently the building has five units; two are leased and the rest are vacant. If fully leased, estimated monthly rent income would be about JPY 530,000, corresponding to a gross yield of approximately 10%.

Urba Property-Level Analysis

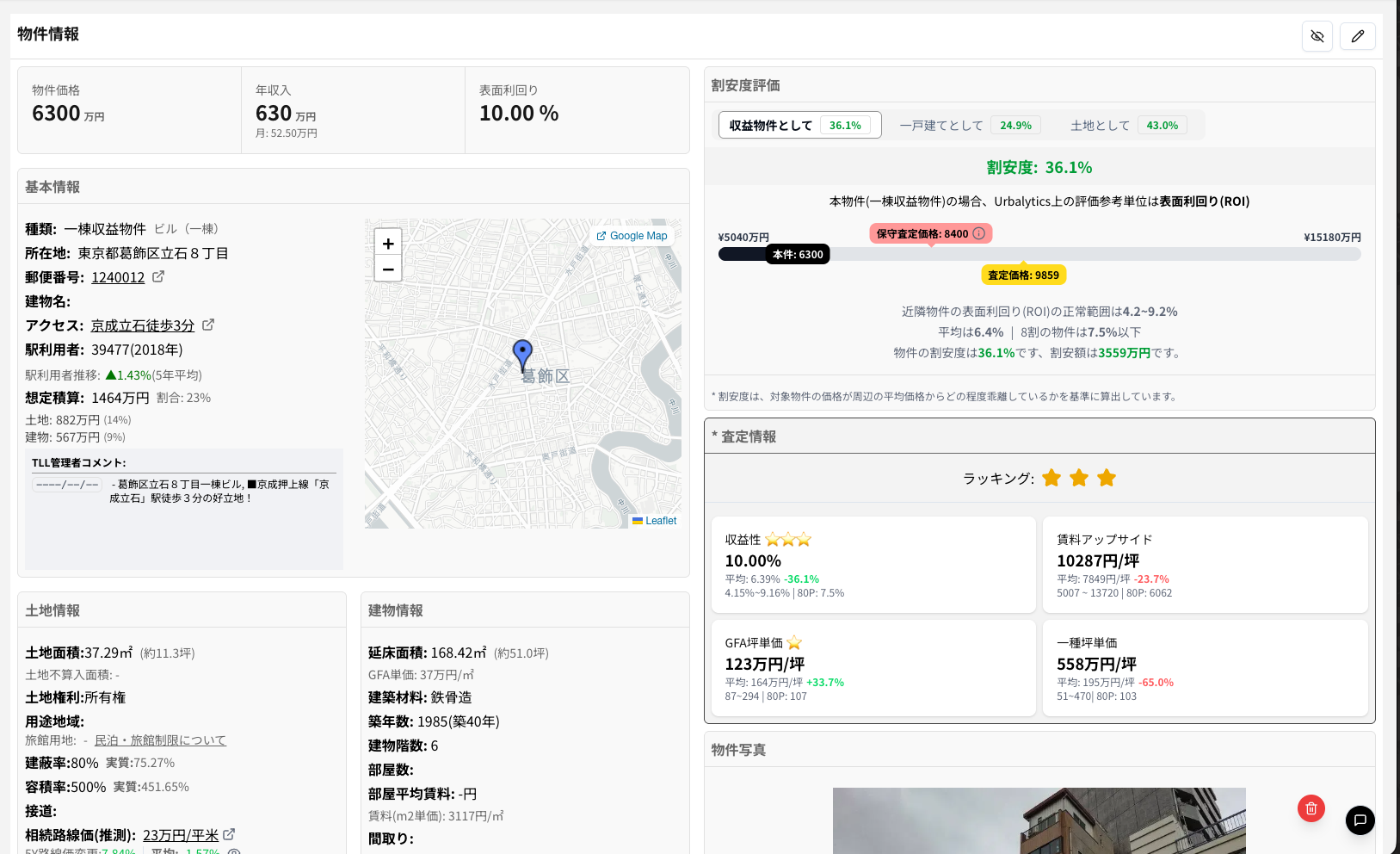

Urbalytics’ valuation indicates that this income property has a discount level of 36.1%. In other words, its price is over 30% lower than comparable income properties in the area.

Based on the current asking price of JPY 63,000,000, the system estimates:

Conservative assessed price of approximately JPY 84,000,000,

Estimated fair price of approximately JPY 98,590,000, which implies a potential discount of about JPY 35,590,000.

By regional comparison, comparable nearby income properties have a typical gross yield (ROI) range of 4.2%–9.2%, averaging about 6.4%. This property’s ROI reaches 10.0%, well above the market average, indicating it is priced low with relatively high yield — a relatively undervalued asset within the income property segment.

❌ Caution — Rents are noticeably high

“賃料アップサイド” (rental upside) normally indicates how much rent can increase, but here it is negative (-23.7%), meaning there is no upside and that current rents are high. This suggests current rent levels may already be near the market ceiling; if a tenant vacates, re-leasing may require rent reductions to maintain occupancy. For investors, this implies:

Short-term cash flow is relatively strong and near-term returns are attractive;

but there is a risk of future rent declines, so long-term sustainability must be assessed.

Given that only two units are currently leased, the seller may have overstated the estimated rent to justify a higher asking price.

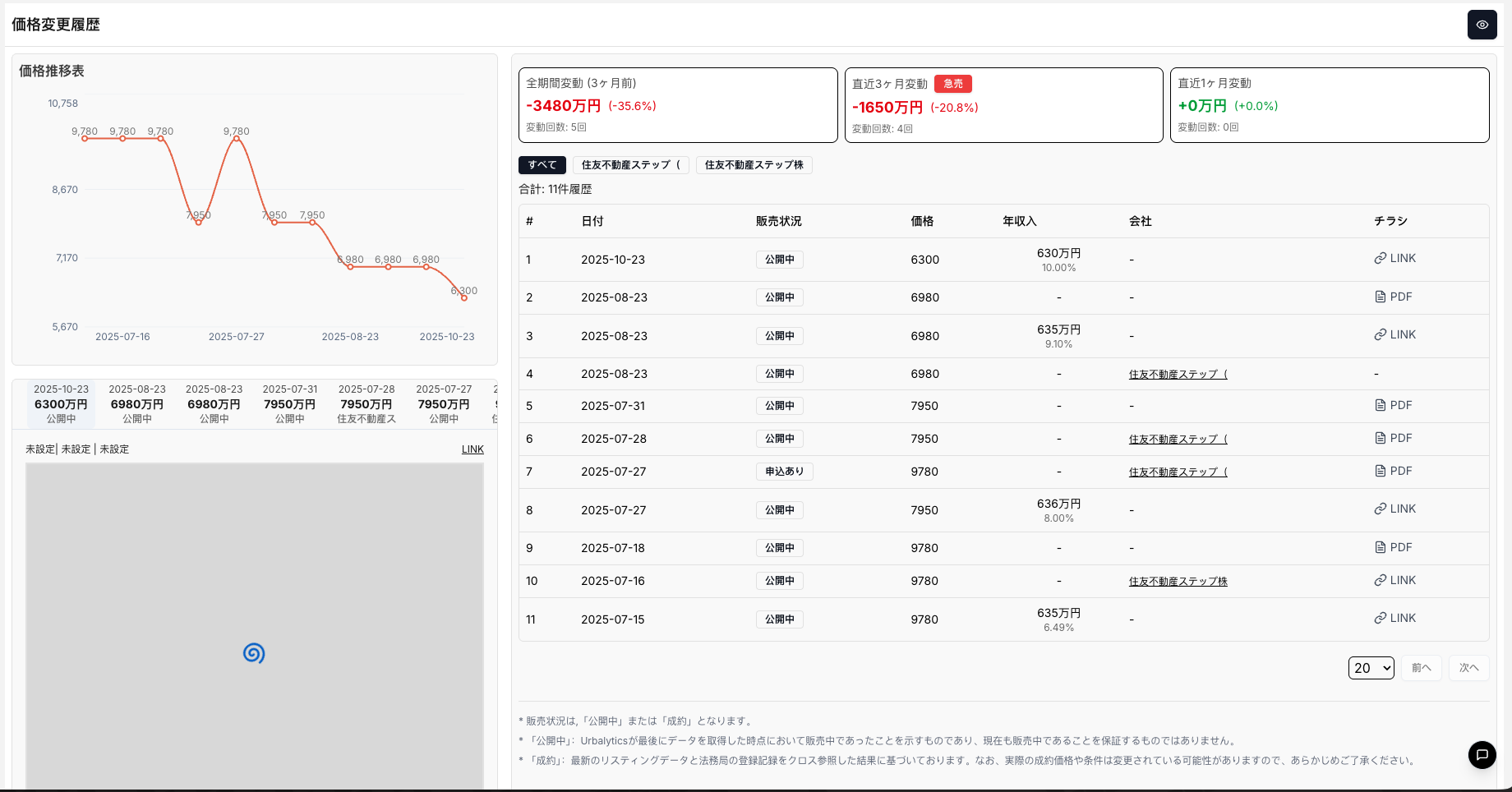

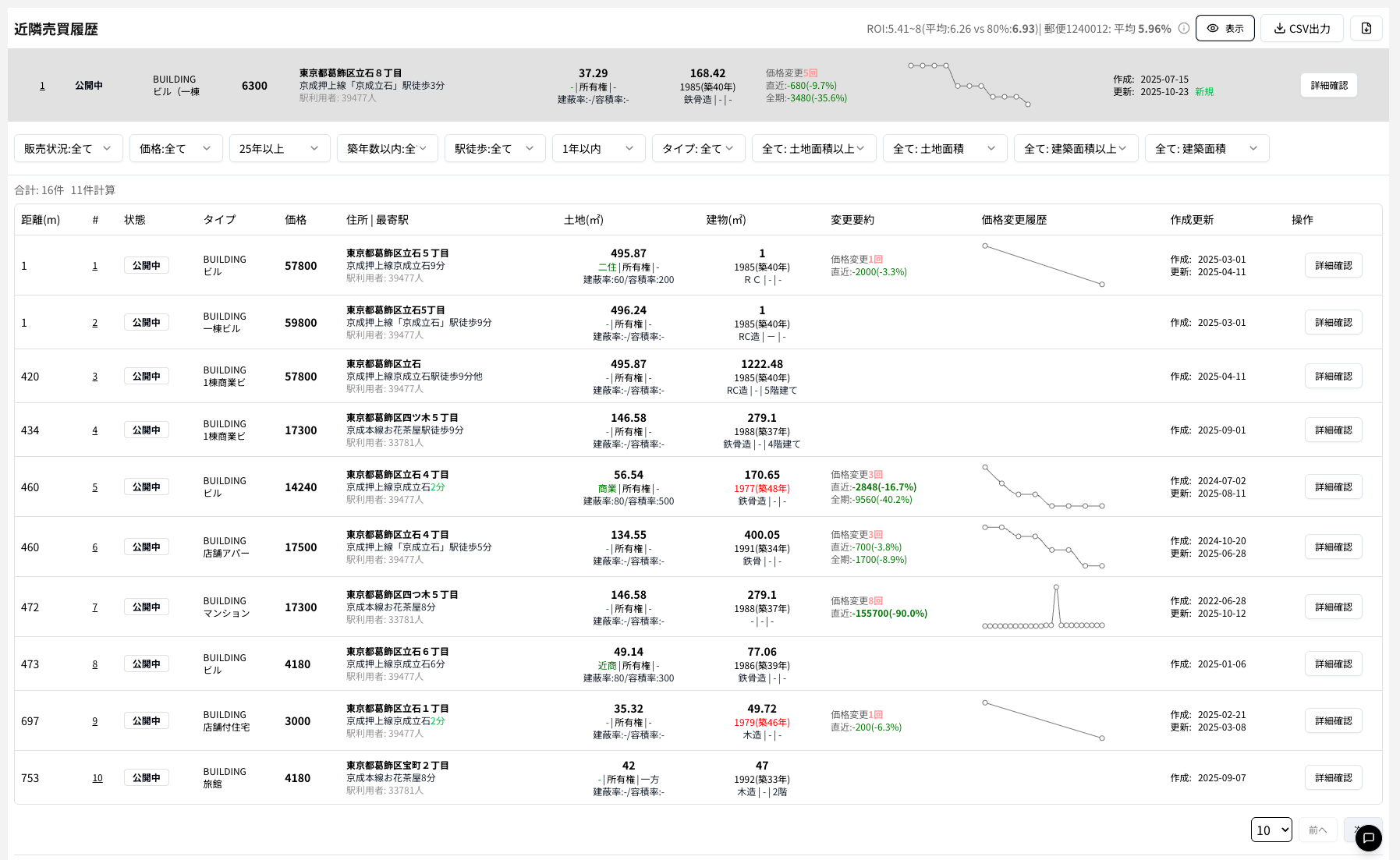

#2 Price Reduction History

Price history shows that this income building in Tateishi has undergone significant price reductions and market repositioning over the past three months. Initially listed in mid-July 2025 at JPY 97,800,000, the price was progressively lowered to JPY 79,500,000 by late July–August, dropped further to JPY 69,800,000 by late August, and was finally set at JPY 63,000,000 on October 23. In just three months the price fell by approximately JPY 34,800,000 (-35.6%), with a decline of more than 20% in the most recent three-month window — a typical "urgent sale" pattern.

Such frequent and large reductions suggest the seller may be under financial pressure or facing vacancy issues, and that the initial asking price exceeded the market’s acceptable range, resulting in weak transactional feedback. Notably, the price has been stable for the past month, indicating the seller may be near their psychological bottom and seeking a sale at the current level.

For buyers, this price trajectory means there is both negotiation room and investment opportunity. The current price of JPY 63,000,000 is well below the market-assessed value, placing the property in a “discount zone.” If the building condition is sound and rent income can be sustained, purchasing now represents a low-entry point with controllable risk.

However, buyers should confirm whether the price reductions relate to building condition, tenant stability, or sustainability of income to ensure the urgent sale is not due to hidden defects (for example, photos show an added rooftop structure — if it lacks approval this could pose safety risks and would require application and removal).

#3 Local Market and Comparable Prices

Local transaction data indicates the income property market around Tateishi in Katsushika is characterized by high asking prices, weak transaction momentum, and continuous repricing. This whole-building in Tateishi 8-chome (current price JPY 63,000,000) sits at the lower end of the local price band and appears distinctly inexpensive compared with nearby similar buildings. Comparable listings in the area are mostly in the JPY 140,000,000 to JPY 60,000,000 range; some larger commercial buildings (e.g., in Tateishi 5-chome) are priced around JPY 57,800,000–JPY 59,800,000 but have land areas near 500 m² — more than ten times this property’s land area. This shows that while the absolute asking price here is low, the price per building area is competitive, representing a "small-lot, high-rise" income profile.

From the top-right indicators on that page, Urbalytics has statistically compared gross yields (Cap Rates) for nearby income properties. The regional average yield is about 6.26%, commonly ranging from 5.4% to 8.1%, while this property’s gross yield is 10.0%, significantly above the regional benchmark.

However, from an investment perspective, a high Cap Rate—while indicating strong on-paper returns—often comes with higher underlying risk. Examples include overheated rent levels, uncertain tenant stability, or elevated maintenance costs. Buyers should therefore treat the high yield as a “risk premium” and only acquire after verifying rent sustainability and confirming the building’s condition to lock in genuine high returns.

4 Rent Analysis

The "賃料アップサイド" (rental upside) analysis shows current rent levels for this property are relatively high within the local market, indicating certain risks and constraints. The system reports the property’s average monthly rent per tsubo as ¥10,300/tsubo, while comparable nearby income properties average about ¥7,800/tsubo, a difference of -23.7%. In other words, the current rents for this property are about one-quarter higher than the local income-property average.

When comparing only whole-building rental properties (so-called "entire-building rental properties"), the gap is even larger: the nearby average is ¥6,200/tsubo, which is -39.5% compared to this property. This indicates current rent levels are far above the local market average for investment properties, meaning rents may be unsustainable and there is downward pressure on rents if tenants change or contracts are renewed.

5 Overall Investment Return Analysis

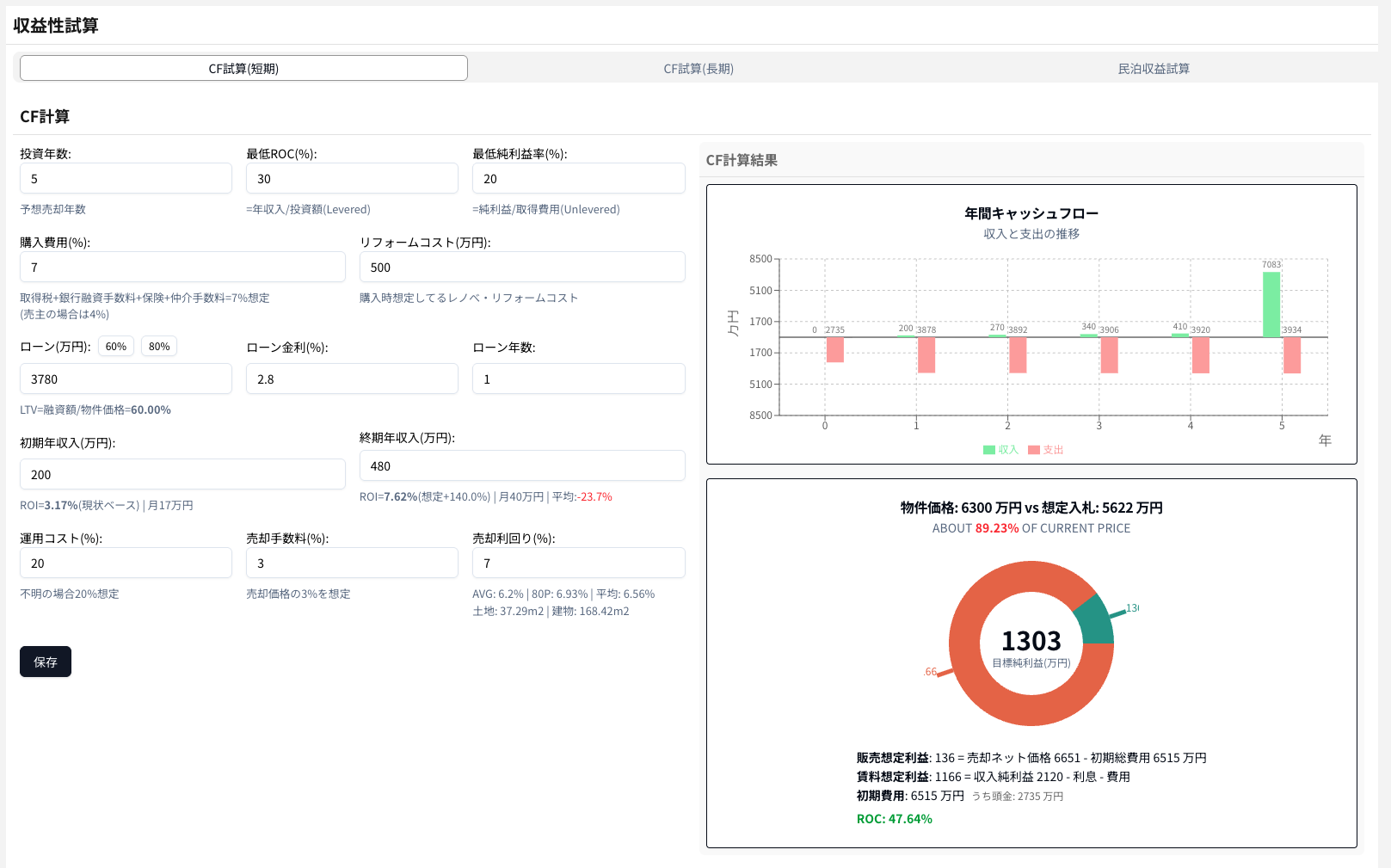

The model assumes a purchase price of JPY 63,000,000, loan-to-value (LTV) of 60%, a loan amount of approximately JPY 37,800,000, interest rate of 2.8% annually, and a loan term of only 1 year. Initial annual income is set at JPY 2,000,000, and income at the end of the period (year 5) declines to JPY 4,800,000, reflecting a rent adjustment (-23.7%). Operating costs are assumed at 20%, sales fees at 3%, an exit horizon of 7 years, and renovation costs estimated at JPY 5,000,000 (restoration to original condition, building demolition costs).

The cash-flow chart on the right shows negative cash flow during the first four years due to loan repayments, operating costs, and rent decline; however, at the year-5 sale (including capital recovery) there is a pronounced positive cash-flow peak, with annual net proceeds of about +JPY 70,830,000, indicating the investment is profitable at exit. The system calculates a projected net profit of approximately JPY 13,030,000, equivalent to a 47.64% ROC (Return on Cost) on the invested capital. If our target ROC is 30%, this meets our investment threshold.

In terms of IRR, to secure a 20% IRR under the above assumptions, the indicative bid price would be around JPY 56,220,000, or roughly 89% of the asking price. Given that the current price has stabilized, achieving a large further reduction may be difficult.

Summary

This six-story income building in Tateishi, Katsushika, is currently listed at JPY 63,000,000 — about 36% below market valuation — with a gross yield of 10%. However, rents are noticeably higher than the regional average and face downside risk. Urbalytics’ model estimates a roughly 47.6% ROC over a 5-year hold. For a target IRR of 20%, a reasonable acquisition price would be around JPY 56,220,000. Overall, this represents a discounted, high-yield investment opportunity that requires careful verification of rent sustainability.

Listing link: https://urbalytics.jp/ex/search/cmd4jvjjr0005pxwkipx5iz1w

If you would like a similar analysis for your property, sign up for a free Urbalytics trial:

👉 https://urbalytics.jp/login?tab=signUp

Or send us your property details and we will prepare a customized report for you 📩