Words: 1242 | Estimated Reading Time: 7 minutes | Views: 2273

Recently, Credit Saison Co., Ltd., together with Mizuho Trust & Banking, Mizuho Bank, Tosei Asset Advisors Co., Ltd., and Securitize Japan Co., Ltd., announced a collaboration to launch Japan’s first real-estate security token (Security Token, ST) issued by a credit card company — “セゾンのスマート不動産投資” (Saison’s Smart Real Estate Investment). The service aims to lower the entry barrier to real estate investment through digitalization, enabling more individual investors to participate in real estate assets.

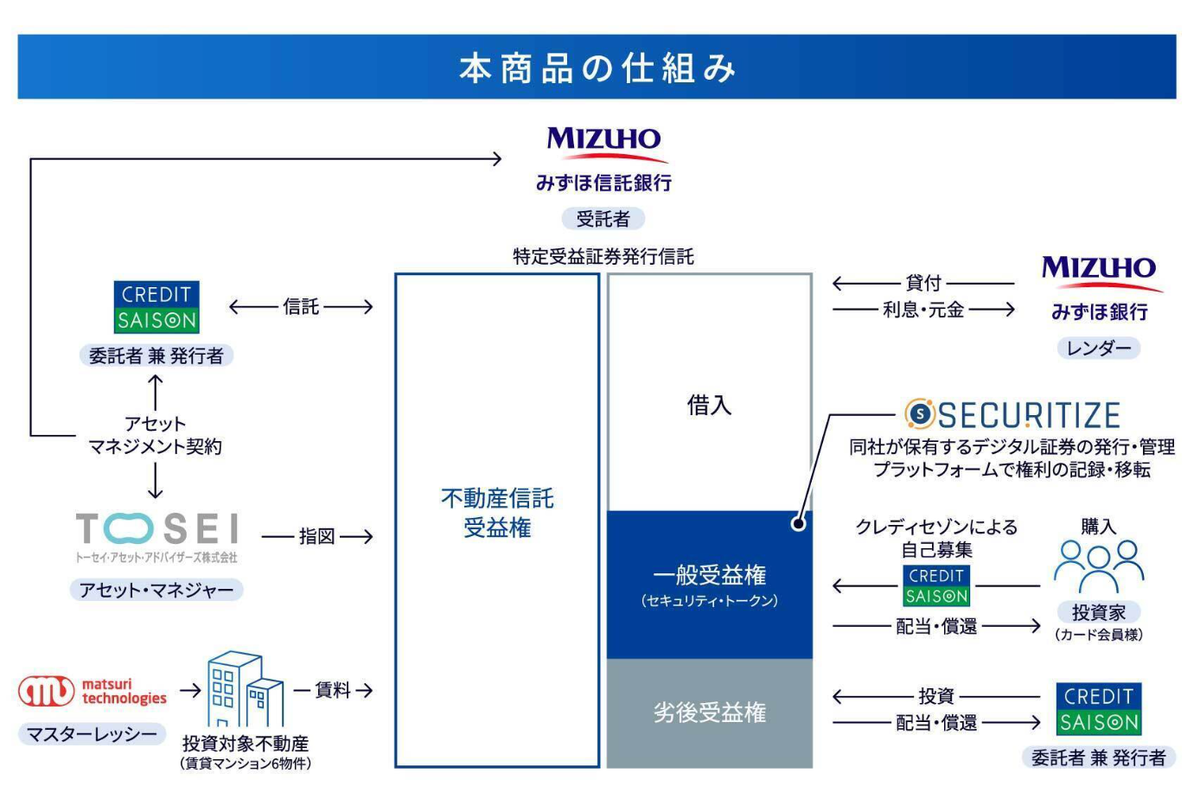

Product structure

Asset origin: Tosei Asset Advisors (asset manager) is responsible for sourcing and managing real estate projects. Real estate assets will be held in trust with a trustee (for example, Mizuho Trust & Banking) to ensure asset independence and transparency.

Beneficial interest structure: divided into:

Senior beneficial interests (the portion available for investor subscription)

Subordinated (junior) beneficial interests (subscribed by Credit Saison to provide a risk buffer)

Fundraising

Investors participate via a blockchain platform provided by Securitize Japan; Securitize Japan is responsible for fundraising and investor registration management.

Investors can use cash or credit-card loyalty points (the program’s non-expiring points) to invest, lowering the participation threshold.

Cash flow allocation and protection mechanisms:

Rental income generated during the investment period and proceeds from final property disposition are collected by the trust and preferentially distributed to senior beneficial interest holders.

If losses occur, the subordinated beneficial interests held by Credit Saison absorb losses first, thereby protecting the principal of general investors.

Financing process: under the trust structure, leverage for asset operations can be obtained via borrowing (for example, loans from Mizuho). After borrowers repay principal and interest, remaining cash is used to pay investor returns.

Highlights promoted on the official website include:

Low minimum investment, low barrier: Investors can participate with as little as JPY 100,000 and do not need to open a securities account. Saison and UC cardholders can also invest using accumulated non-expiring loyalty points, starting at 200 points (approximately JPY 900), in 100-point increments — flexible and convenient.

Risk control: senior–subordinated structure: The product uses a senior–subordinated design; if the investment property incurs losses, Credit Saison, as the subordinated investor, will absorb losses first to maximize protection of ordinary investors’ principal.

Clear investment targets and asset visibility: Unlike traditional J-REITs, Saison’s Smart Real Estate Investment targets specific real estate projects — for example, properties within Tokyo’s 23 wards such as Kagurazaka, Waseda, Nishi-Waseda, Sugamo, Omori, and Omorimachi — allowing investors to clearly understand the assets they are investing in.

Regulatory backing and technical safeguards: The service is based on the 2020 revisions to the Financial Instruments and Exchange Act, which clarified the legal status of security tokens as financial instruments, strengthening legal protections for investors. At the same time, blockchain technology is used for electronic issuance and management of tokens, improving transaction transparency and security.

State of Japan’s crowdfunding market: concerns amid rapid expansion

In recent years, Japan’s real estate crowdfunding market has expanded rapidly, with annual inflows surpassing JPY 100 billion. Characterized by “small-ticket, online, high-yield” offerings, these products have attracted a large number of individual investors seeking exposure to real estate. However, as a culture of “yield-centric” marketing has spread, some operators have attracted capital by promoting projects with advertised annual returns exceeding 10%, but in practice have faced delays in asset management and exit, payment difficulties, and opaque use of funds, challenging investor confidence. For example, the payment delay controversy surrounding Yamawake Estate exposed weak risk controls and insufficient transparency at some operators, prompting strong reflection from regulators and industry associations.

According to reporting by Rakumachi, many platforms use large fonts and bright colors to attract investor attention, overemphasizing “high yields” in marketing while failing to adequately explain potential risks and the use of funds. Representatives from the Small-lot Real Estate Association note that many investors lack basic investment literacy and do not fully understand the principle that “higher returns imply higher risk,” making yield-centric strategies a structural issue. At the same time, some platforms lack contingency plans when assets cannot be exited on time; if a buyer’s financing fails or the market weakens, payment delays or funding shortfalls can occur. These warning signs are very similar to the problems early social-lending platforms encountered; without stronger regulation and investor education, the industry risks repeating past mistakes.

The “Yamawake” issue exposes industry risks

In early 2025, the well-known real estate crowdfunding platform Yamawake Estate experienced a series of payment delays that raised investor alarm and became a catalyst for industry-wide reflection and reform. The incident revealed that even projects operating under the Act on Specified Joint Real Estate Ventures can suffer from unrealistic return projections, unclear repayment plans, and weak investor protection mechanisms.

Industry associations have indicated they will promote standardization with a stronger sense of urgency to prevent a recurrence of “high-yield inducement + weak risk control.” Given market fluctuations and potential buyer financing failures, project repayment always carries risk; lacking transparent disclosure and emergency mechanisms will significantly damage investor confidence.

Saison ST model: real-estate securitization × consumer finance — the next step

Against the backdrop of a growing trust deficit in Japan’s small-lot real estate investment sector, the joint launch of Saison’s Smart Real Estate Investment by Credit Saison and four partners offers the market a potentially safer solution. As Japan’s first publicly offered real-estate security token (ST) led by a credit-card company, the service combines the low minimum investment advantage with consumer-finance features such as non-expiring points investment and no-account-required participation. The senior–subordinated structure effectively protects ordinary investors’ interests, and the product design demonstrates stronger compliance and risk-control awareness.

This model stands in sharp contrast to recent crowdfunding incidents like the Yamawake case. Although those platforms also claim “high returns” and “small-ticket participation,” unclear operator responsibilities, insufficient risk disclosure, and opaque exit mechanisms have led to frequent repayment delays and even principal risk for investors. The ST model, subject to the Financial Instruments and Exchange Act, requires filing securities registration documents and benefits from trust mechanisms and blockchain-based recordkeeping, resulting in far higher information transparency and legal compliance than typical crowdfunding offerings.

Fundamentally, STs are regulated, registered, and tradable financial instruments, while many crowdfunding products operate as simplified-permit joint-investment structures. The two differ markedly in legal status, disclosure obligations, and investor protection mechanisms. The rise of STs suggests that Japan’s small-lot real estate market may be shifting from a yield-driven approach toward a model emphasizing structural safety and transparent trust, potentially triggering a new industry reshuffle.

Closing remarks

By combining fintech with traditional credit systems, Saison’s Smart Real Estate Investment provides a new pathway for small-lot real estate investment in Japan. It breaks the conventional perception of high entry barriers, and through mechanisms such as point-based investment and a senior–subordinated structure, balances inclusiveness with risk control, opening a new avenue for personal wealth management.

For first-time real estate investors, it offers a low-barrier, low-complexity entry point; for experienced investors, it provides a tool for portfolio diversification and hedging against traditional market volatility. As financial products continue to digitalize and securitize, ST-type offerings are expected to accelerate in the coming years and may become one of the more compliant and transparent mainstream solutions in the post-crowdfunding era, warranting long-term attention and study.

References

https://st.saisoncard.co.jp/service/?utm_source=chatgpt.com — How the service works

https://www.rakumachi.jp/news/column/367624 — “Yield bias” as a breeding ground for trouble: challenges in real-estate crowdfunding as annual inflows reach JPY 100 billion

https://www.kenbiya.com/ar/ns/release/p_service/9017.html — Credit card company launches real-estate security token “Saison’s Smart Real Estate Investment”; five companies begin collaboration